In 2023, PiggyVest launched its first national savings report. The sample then covered a meaningful but limited cross-section of Nigerians. Two years later, the methodology has expanded considerably.

The 2025 edition surveyed over 26,000 Nigerians across 12 states, encompassing all six geopolitical zones and reaching urban, peri-urban, and rural settlements for the first time on a large scale.

Field researchers conducted in-person interviews. Structured questionnaires were administered via Open Data Kit in English and local languages. The sample comprised salary earners, small business owners, students, and members of the general public, with ethical clearance obtained from the FCT Health Research Ethics Committee before data collection.

This is not a fintech platform pulling numbers from its own user base. It is the closest thing Nigeria currently has to a nationally representative consumer financial health survey conducted at this frequency. And the picture it delivers, with all that expanded reach, is more alarming than the two editions that came before it.

Savings drops to 40% – PiggyVest

In 2023, 64% of survey respondents said they saved monthly. By 2024, that figure had dropped to 47%. In 2025, it fell again to 40%. The share who report saving occasionally has also declined, from 15% in 2023 to 7% in 2025.

The share who report not saving at all has moved in the opposite direction, rising from 21% in 2023 to 43% in 2024 and settling at 53% in 2025. More than half of Nigerians surveyed, in a sample that now spans the full geographic and demographic width of the country, do not save.

The three-year trajectory matters more than any single year’s number. It shows a trend that predates and outlasts the specific economic shocks of any given moment.

Annual average inflation surged to 31% in 2024 due to naira depreciation, food supply deficits, energy subsidy removal, and high borrowing costs. That is clearly part of the explanation. But the decline in savings began in 2023, before inflation peaked, which means the erosion of savings capacity started earlier and ran deeper than a single-year shock can explain.

The barriers that non-savers themselves identify make the picture clearer. Among those who report not saving, 60% say they simply do not earn enough. Another 21% say they do not care about saving, and 19% say they do not know how to save.

The income constraint is dominant, but it is not the whole story. More than 57% of those who say they cannot afford to save report having no monthly income at all, followed by 29% earning below ₦100,000 monthly. These are not people making trade-offs between saving and spending. They are people for whom saving is structurally impossible, given what they earn and what basic life costs.

EFInA’s research described the underlying condition bluntly: the system has laid the pipes of access but not the lifelines of resilience. Formal credit stands at 9%, insurance uptake is just 3%, and accounts are used overwhelmingly for payments rather than for building buffers against shocks. The PiggyVest data lands in that context and confirms it from the demand side. Financial tools exist. The conditions that would make using them viable for most Nigerians do not.

The emergency fund data reinforces the savings trend. 6 in 10 respondents report having no emergency funds set aside. Among those who do have emergency savings, the majority can cover only 1 to 3 months of expenses, and only 15% have funds that would last six months or more, the minimum threshold most financial planners recommend. Compared with last year, many respondents say their emergency buffers have declined or disappeared entirely.

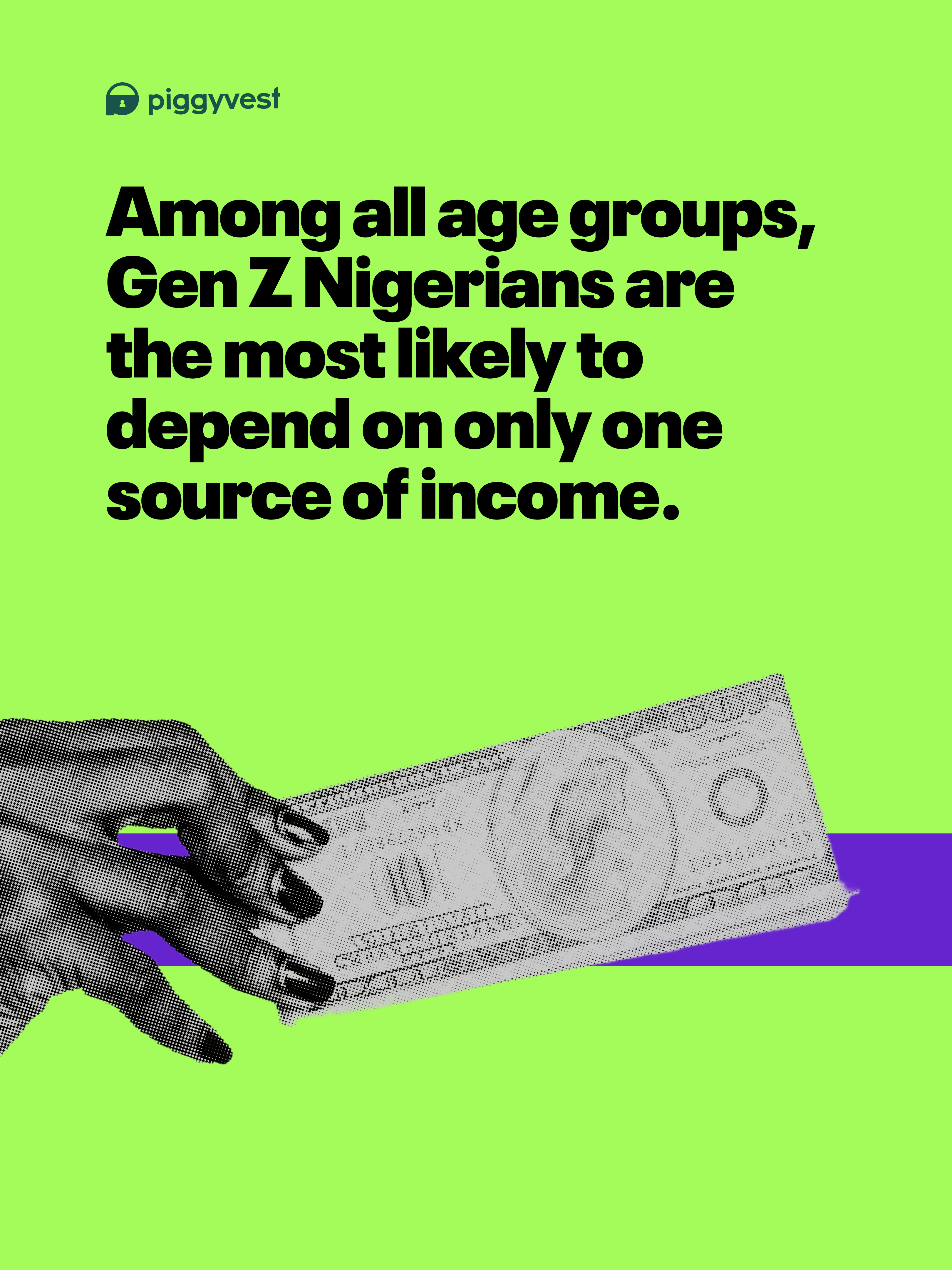

The generational split within this data deserves attention. Gen Z Nigerians, those between 18 and 28, are the least financially protected of any cohort.

Only 31% report having any emergency savings, compared with 52% of Gen X respondents. Gen Z is also the most likely generation to depend on a single income source, at 74%, and the most likely to earn below ₦100,000 or report no income at all.

These are the Nigerians entering the labour market and early adulthood in an economy where, as PiggyVest COO Odun Eweniyi puts it, inflation peaked above 33% in 2024, and people are earning more and affording less.

The World Bank’s October 2025 Nigeria Development Update acknowledged the paradox directly: macroeconomic gains have yet to translate into tangible improvements in people’s lives, with poverty and food insecurity remaining high.

The PiggyVest data measures the household-level consequence of that gap. GDP is growing. Savings are collapsing.

What makes the 2025 survey significant beyond its findings is what its methodology confirms. Piggyvest went further into rural Nigeria than any previous edition, reaching populations that fintech platforms rarely touch and that previous surveys under-represented.

The expanded sample did not surface a more optimistic picture of savings behaviour. It made the picture more complete and, in doing so, more damning. A savings crisis that looked concentrated and urban in earlier readings turns out to be broad, geographic, and structural.

Nigeria’s financial inclusion headline tells one story: financial inclusion rose to 74% in 2023 from 68% in 2020. More Nigerians have accounts than at any point in the country’s history. The PiggyVest data tells the companion story: having an account and using it to build financial resilience are two different things, and for the majority of Nigerians, the second is becoming harder, not easier, with each passing year.