In 2018, I first experienced just how difficult it is to verify an address in Nigeria.

It was a hot Wednesday afternoon and I remember scribbling numbers into my diary when an unknown call came in.

“My name is Isaac from X bank, I have come to verify your address. Are you home?” the person at the other end asked.

What followed was a 20-minute conversation where I had to explain that I was at work and won’t be available just so he wouldn’t give a negative verification. What surprised me most is the fact that he told me he was booked for the whole month, when I asked to reschedule. I ended up finally doing the verification 3 weeks later.

Like me, thousands of Nigerians have had to weather the discomfort associated with verifying addresses. However, the challenges associated with verifying physical addresses aren’t exactly caused by banks or businesses.

Every month, banks and businesses onboard hundreds of thousands of new customers that need address verification as part of Know Your Customer (KYC) requirements and they are running a very inefficient process.

In a chat with Technext, Galen Crawley, Chief Commercial Officer, OkHi, a Smart Addressing Platform explained the challenges businesses face with address verification and how smart systems help solve them.

He explained that what is lacking in the current process is that it is still manual. It involves people and documents that can be cumbersome if you consider the large number of customers being onboarded.

According to him, replacing the process with a smart system through a business app unlocks the ability for all financial services to do all of their KYC digitally including the addressing part, making it easier and faster.

Why is KYC important?

The verification of identity or Know Your Customer (KYC) is a process new users and business have to deal with. While the process is a compulsory requirement for businesses to onboard customers, it is often an unwelcome chore for new users.

Galen explained that the importance of KYC is more for the business. “KYC literally means Know Your Customer and that translates into trust. If you can trust your customer you can offer them more and better services.”

However, the Central Bank of Nigeria says it’s important because it helps check risk and determine whether or not there is an element of money laundering, fraud and other corruption-related activities.

As a business expert, Galen agrees with the regulator. He believes that knowing where someone lives is an important part of their identity and trusting who they are.

For example, if a bank or a fintech wants to offer someone money or a loan, they need to trust them. They need to know where they live. Otherwise, the risk is too high.

Galen Crawley, Chief Commercial Officer, OkHi

The different types of KYC

There are several types of processes used for KYC, from identity card verification to address verification and biometrics.

Asked if one was superior to the other, Galen explained that they are all used for different purposes in a sense and are not comparable in terms of value.

“For example, address verification becomes an important requirement when you are serving a tier 3 account customer, it doesn’t for a tier 1. For tier 1 you might need to do biometric identity verification,” he added.

Why Smart Addressing is better than Older Methods

Focusing on address verification, the current method businesses use nowadays is paper-based. They get the customer to write down their address, street name and number. However, this method in itself is quite inaccurate if an addressing system doesn’t exist.

Mr Crawley explained that there are few options business use to verify this method. One is to get utility bills for that address. This is, however, a problem because lots of people don’t have utility bills and if they do, it’s often not in their name – so it is a painful and unreliable way to verify an address.

The other as I narrated earlier is the use of agents to verify the address physically. The problem with this method is that it’s extremely expensive and unscalable, and can also be painful for the customer. The problem with both is that if someone moves addresses at any point, the previous address becomes out of date therefore useless. It’s a broken system. For that reason, he pointed out some businesses avoid it altogether, putting them at risk.

However, several tech innovations are being created to improve the process. The Nigeria Postal Service (NIPOST) has created an Address Verification System (AVS) to bridge the physical addressing gap in Nigeria.

The AVS platform is an upgrade from the old agent-based system which employs paper details. The platform is designed to allow the agents to sign in, geo-tag and take pictures, thereby generating a digital address for anywhere in Nigeria to be verified.

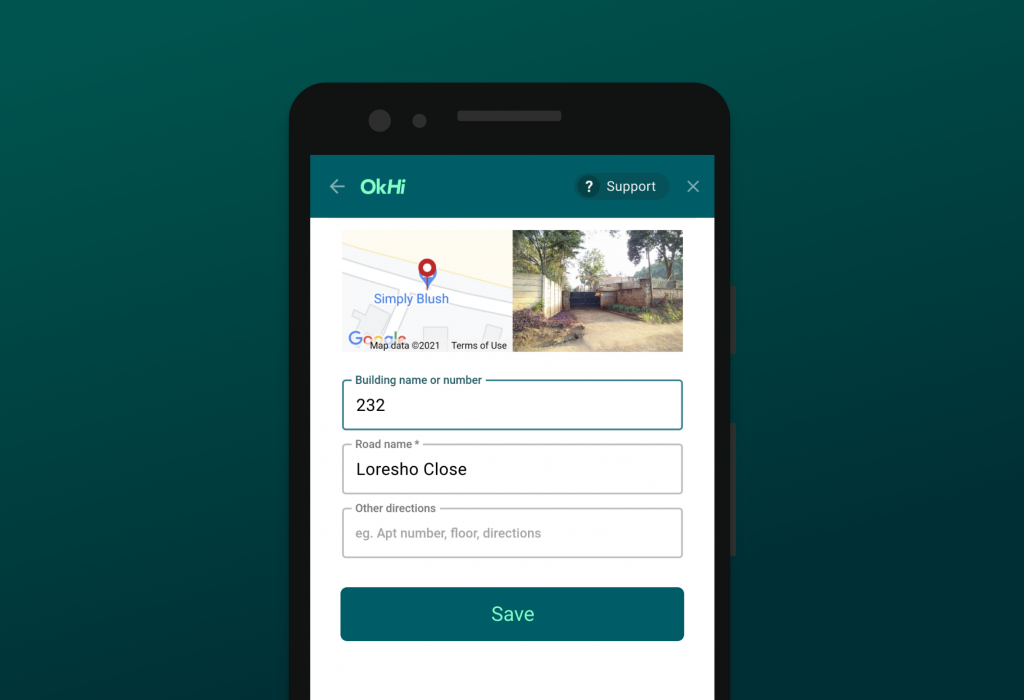

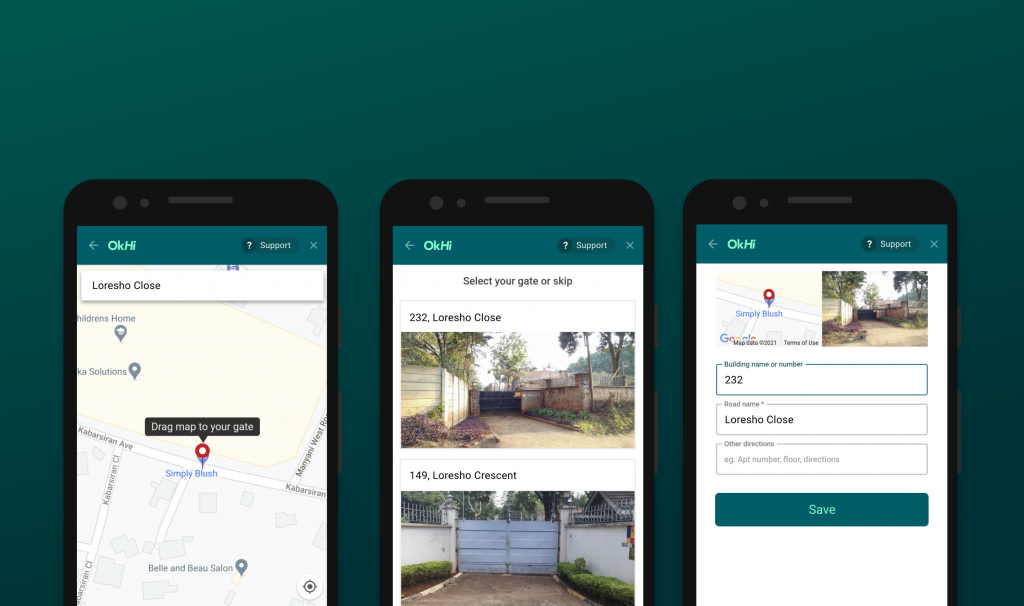

Another breakthrough is the digital address verification system created by OkHi. It is the first of its kind and it enables businesses to collect addresses from the customer and verify them easily without agents.

All the customer needs to do is drop a pin on the map on the address collection product just like uber, click on their gate photo using google street view and type in the text instructions and their address is created. The verification is done by matching their phone GPS against their OkHi address.

This means that agents may lose their jobs but it also presents a lot of ease for both business and customers.

According to Galen, this essentially verifies their address digitally and remotely so that neither the customer nor business has to do anything.

Asked what happens when an area has no official address system, OkHi’s Chief Commercial Officer says it’s possible to essentially eliminate the need for street names and numbers.

He explains that the GPS point with the dropping the pin is an equivalent of a street address, the photo of the entrance of the building is like a street number and the text instruction saying something like Apartment 4A gets someone at the front door.

“GPS + Photo + text directions makes the address 100% accurate”

Galen Crawley, Chief Commercial Officer, OkHi

Galen says that the new verification product is about to go live with Quickteller, Kuda Bank and other prominent fintechs.

Lower onboarding rate and faster scaling

When the CBN banned the use of BVN for KYC verification, the cost of onboarding users through other alternatives like address verification were some of the concerns raised by businesses.

According to Mr Crawley, sending an agent to verify an address costs between $3 – $5 (around N2,000). But the OkHi system is significantly cheaper than that and much more scalable.

He explained that businesses can use their product by integrating it into their app. He added that they need to have a mobile app because the verification system uses the business app.

The integration or onboarding process takes about a day or 2 technically but can be shorter depending on the business capacity and team resource.

With an OkHi integration, businesses can collect and verify their customer’s addresses all within their app.

For those that don’t have an app, Galen says they can use the OkHi app on Playstore, which can collect and verify addresses.

OkHi has a partnership with Interswitch to help market its verification system among its wide client base. Interswitch was a key investor in its latest fundraising round of $1.78m.

In summary,

Smart addressing makes it easy for businesses to verify their customer addresses through their smartphone and replace the need for utility bills and physical visits.

Galen believes the future of KYC (biometrics and address verification) is fully digital. He explained that the future is very close as companies like Smile Identity are providing digital identity verification through biometrics. And OkHi has now solved the digital address verification part, where anyone can essentially verify who they are using their smartphone.