Jumia, Africa’s e-commerce giant, has recorded more losses than profits during the second quarter of the year.

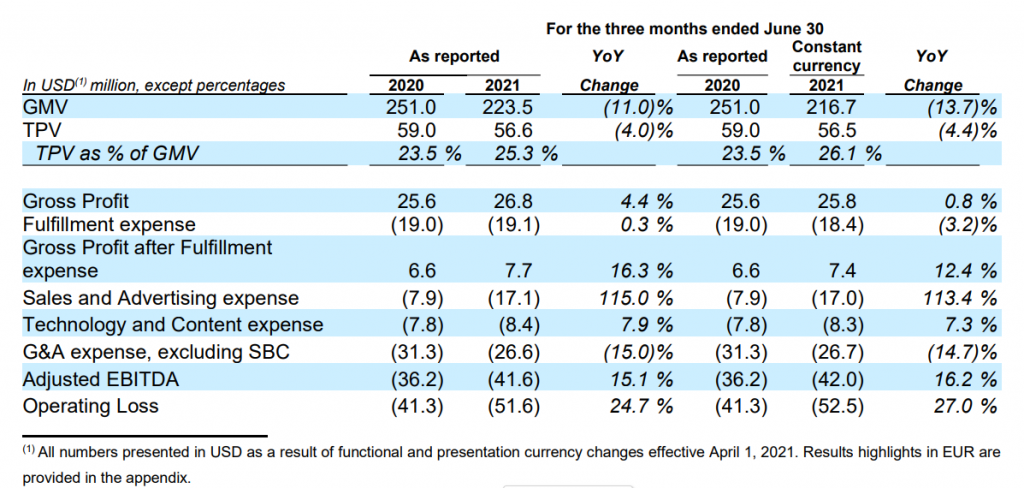

According to its Q2 earnings report, operating losses rose to $51.6 million, up 24.7%, overshadowing its gross profit which grew just 4% to $26.8 million during the quarter.

The report shows a slight tweak in the company’s growth strategy as a whopping $17.1 million was spent on sales and advertising during the quarter.

According to Jumia co-CEOs, Jeremy Hodara and Sacha Poignonnec, the increasing sales and advertising investments are part of the company’s plans to leverage the boost gotten from its change in business strategy.

In 2020, Jumia tweaked its business model to focus more on its third-party marketplace, where it collects a commission on items listed and sold on its platform instead of its first-party model, where it had to buy stuff and sell.

However, the increased spend on marketing which consequently increased losses hasn’t instantly translated to a huge boost in profit as seen in the report.

Despite the increasing losses, Jeremy and Sacha say that they have started to see early signs of usage acceleration which will lead to significant growth in the long run.

“While we start to see early signs of usage acceleration, these investments are long term in nature and we expect them to pay out over time, as we continue to execute on our strategy,” they said.

Food delivery drives growth in number of orders

A look at the company’s growth during the quarter shows Jumia added up to 200,000 new active customers to reach 7 million confirming the co-CEOs claim of usage acceleration.

However, it appears that order numbers were the major benefactors of Jumia’s aggressive marketing. Orders on the platform increased 12.8% from last year to 7.6 million.

A breakdown shows that food delivery saw explosive growth, accounting for 22% of total orders while phones and electronics have continued to decline. Fast-moving consumer goods (FMCGs) like groceries continued to grow albeit slightly.

Food delivery rose 60% year-over-year to post its highest ever number of quarterly orders

Gross Merchandise Volume (GMV) on the other hand, declined 11% from $253 million in Q2 last year to $223.5 million during the same quarter this year. However, it was still a huge improvement from $200 million recorded during the first quarter of the year.

The report shows that consumer electronics and gadgets accounted for 37% of Jumia’s GMV, while FMCGs accounted for just 14%.

Subsequently, Jumia’s falling GMV impacted the total payment volume (TPV) of JumiaPay, as the total volume dropped 4% to $56.6 million during the quarter.

Despite the drop, JumiaPay’s results were impressive. Its transactions grew by 12% from 2.4 million last year to 2.7 million. Also, its on-platform penetration grew to 23.5% in the second quarter.

Over $40 million in Revenue

Generally, the increase in orders pushed Jumia’s revenue to rise 4.6% on a year-over-year basis to $40.2 million.

The revenue generated failed to meet analysts’ expectations of $43.34 million but it marked a significant growth from the $33 million generated during the first quarter of the year.

A breakdown shows that its first-party revenue increased 7% in the second quarter more than the 0.6% growth seen in the marketplace for third parties despite the shift in focus.

The marketplace generated a total of $26.2 million more than half of Jumia’s revenue for the quarter.

In terms of profits, Jumia’s gross profits after fulfilment expenses have been positive, continuing the trend of the past six quarters. The revenue shift further boosted its growth as profit was up 16.3% to $7.7 million. It also marks a linear growth from the $7.5m recorded in Q1 2021.

In summary

Jumia has changed the currency it uses in its report from the Euro to the US dollar going forward. According to the company, the increases in cash balances from equity fundraising was the main reason behind the change.

That aside, the huge increase in sales and advert spending may indicate that the company is back to its old method of executing aggressive advertising.

The company’s current rising operating costs and low profitability are not encouraging in terms of near-term profitability.

However, it appears that investors are content with its current progress as Jumia shares rose 3.38% to $21.99 per share with a market cap of $2.168 billion following its earnings report.