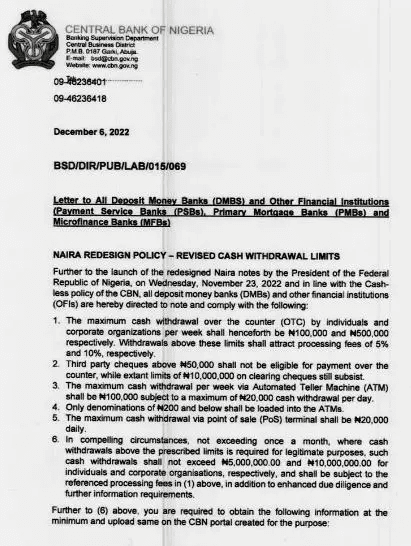

Nigeria’s apex bank, the Central Bank of Nigeria (CBN), has announced a new policy that limits weekly cash withdrawals by individuals and corporate bodies to ₦100,000 and ₦500,000 respectively.

This was contained in a circular to Deposit Money Banks (DMBs) and financial institutions and will take effect nationwide on January 9, 2023.

All cash withdrawals in excess of the stated limits will attract processing fees of 5% and 10%, respectively.

This is coming six years after deposit money banks (DMBs), under the Bankers Committee, approached the CBN to propose a ₦10,000 limit on over-the-counter withdrawals, per Vanguard.

At the time, multiple reports stated that the DMBs wanted to achieve two things: greater use of electronic banking and a smaller workforce – as a means of cutting the cost of operations, considering that unaudited Profit Before Tax of banks for the period ended April 2016 indicated a decrease from ₦222 billion in April 2015 to ₦198 billion, representing a 10.8% or a ₦24 billion decrease.

For the latest instalment of #streetTech, Technext took to the business areas of Lagos, Nigeria to interact with POS agents to get their take on the latest withdrawal limits proposed by the CBN. Many of them claimed that the limit will not favour their business and that the apex bank should reconsider.

One of the agents who spoke to Technext said; “Definitely, it’s going to affect the business. and I belive people like us (POS agents) can always get more funds from the bank because they always see us everyday when we come to make transactions. So for us, it may be easier than for others”

Another POS agent was less calm about the new policy and how it would affect her business.

“That is madness, madness. How can we be withdrawing 20000 Naira everyday? Do you know how much I withdraw everyday? 150000 Naira! so minus the five per cent, how much is that? That is impossible, it will affect my business”

Watch the full video below:

Read also: StreetTech: Are laptop engineers appreciated enough?

Backstory

You would recall in 2019 when the CBN announced new charges on cash deposits and withdrawals on individual and corporate bank accounts. The bank said daily individual cumulative or single cash withdrawals in excess of ₦500,000 would attract a 3% charge, while 2% would be paid on deposits above the amount. For corporate bodies, the benchmark is ₦3 million — 3% for deposit and 5% for withdrawal.

But, the charges do not apply on the first ₦500,000 for individuals and ₦3 million for corporate bodies. They will apply to the excess.

The CBN said the move would encourage Nigerians to handle less cash and instead embrace digital transactions. This was in tandem with the cashless policy announced earlier. One of the key reasons for the cashless policy is:

To drive development and modernisation of our payment system in line with Nigeria’s vision 2020 goal of being amongst the top 20 economies by the year 2020. An efficient and modern payment system is positively correlated with economic development, and is a key enabler for economic growth.

Before then, in 2015, DMBs reduced withdrawal limits on Automatic Teller Machines (ATMs) and foreign transactions on all existing Naira debit cards (ATM cards).

All ATMs formerly enabled for domestic and foreign transactions were restructured to limit Naira cash withdrawal at ATMs to ₦60,000 per day while foreign currency was pegged at $300 per day – the domestic withdrawal limit was ₦150,000 per day.

Also, the restructured cards had spending limits on POS/eCommerce (online shopping) pegged at $300 (about ₦60,000) per day.

Understanding the new policy

This new policy is coming a few weeks after President Muhammadu Buhari unveiled new Naira notes. Still, the new charges will not apply on the first ₦100,000 for individuals and ₦500,000 for corporate bodies. They will apply to the excess amount and is in line with the Naira redesign policy.

According to a new memo to banks issued on Tuesday and signed by the Director of Banking Supervision, Haruna .B. Mustafa, individuals will only be able to withdraw ₦100,000 per week (from over-the-counter, Point of Sale Machines or the Automated Teller Machines), while organisations can access ₦500,000 per week.

But there is a clause.

The memo says that in compelling circumstances, not exceeding once a month, when there are legitimate purposes to exceed the limits, the cash withdrawals will be in the range of ₦5 million for individuals and ₦10 million for corporate accounts.

Banks have also been directed to load only ₦200 and lower denominations into their ATM.

Aiding and abetting the circumvention of this policy will attract severe sanctions - CBN

How will PoS/Online transactions code this?

Before the introduction of the cashless policy by the CBN in 2011, Nigeria’s economy was heavily cash-oriented in its transaction of goods and services, contrary to global trends. So, Point of Sale (PoS) and internet transactions have always been focal points of the cashless policy, such that when PoS transactions fail, there is an outcry.

E-banking improves the time within which transactions are settled both locally and internationally.

Interestingly, PoS transactions in Nigeria increased by 24.3% to 878.4 million in the first nine months of 2022 from 706.8 million in the same period of 2021., indicating that more Nigerians went cashless. Its value also increased by 32.6% from ₦4.6 trillion as of September 2021 to ₦6.1 trillion this year.

Meanwhile, according to the Central Bank of Nigeria 2019 National Financial Inclusion Strategy document, a total of 568,488 additional PoS terminals were deployed from January-September as the number of deployed machines stood at 915,519 as of December 2021.

Mobile transfers also increased as their volume in the first nine months of 2022 amounted to 438.3 million, a 132.3% increase from what was recorded in the same period of 2021 at 188.7 million. In terms of value, it recorded an increased rate of 152.9% year-on-year from ₦5.1 trillion to ₦12.9 trillion. This contrasts the volume of cheque transactions that fell by 6.1% to 3.1 billion from 3.5 billion over the same period.

The volume of Nigeria Instant Payment (NIP) platform transactions also rose to 3.6 billion in the nine months, showing a 50% increase from 2.4 billion recorded in the same period last year.

Over the years, NIBSS says Nigerian banks have exposed NIP through their various channels, including internet banking, bank branch, kiosks, mobile apps, USSD, POS, and ATMs, to their customers.

Bottomline:

The NIBSS says, “there is an increased use of digital channels for transactions and mobile payments,” meaning that there are expectations of increased use over time, especially because of the new charges on excess over-the-counter withdrawals as currently stipulated.

Read also: E-payment transactions rise to ₦32.8trn in September 2022- NIBSS

But “this new policy may kill PoS businesses who rely on commercial banks for cash,” Omotola Collins, a former banker, said.

PoS agents go to banks for cash to service customers who want to pay artisans like bricklayers, carpenters, etc., who do not have bank accounts or are weary of commercial banks in Nigeria. These include customers who want to do big buying in local markets and will meet traders who are still unbanked.

“So, while online transactions will increase, we are looking at the decrease in PoS agents.”

The ultimate idea of the cashless policy is to encourage digital payment systems and increase financial inclusion – which, in turn, aims to reduce poverty – and while there are upsides to every policy, there is always a downside. The CBN is focused on the former.

But not everybody is keen on using smartphones, which will aid the increase of online transactions. Besides, there is yet a substantial distrust of digital methods of transactions among many Nigerians.