A recent Disrupt Africa report found that Nigeria has the largest concentration of fintechs on the continent. In the report “Finnovating for Africa”, the West African country occupies the majority of the market share (32%) with 217 startups. This is not entirely surprising given that Nigeria has established itself as a breeding ground for fintechs.

The country is home to popular names like Kuda, Flutterwave, Opay, PalmPay, and Moniepoint. South Africa (20.6%/140 startups), Kenya (15%/102 startups), and Egypt (9.6%/65 startups) occupy second, third, and fourth places respectively. Ghana, Uganda, Zambia, Senegal, Cameroon, and Rwanda make up the top 10 list.

The big three, Nigeria, South Africa and Kenya account for 67.7% of the market share. When Egypt, Ghana, and Uganda join the mix, the joint stake becomes 86.7%. From this, it is safe to state that fintech activity remains concentrated in the major markets. While the big three attracted the bulk of funding, they also witnessed the most startup exits within two years, Here is a breakdown: South Africa (31.3%/36 startups), Kenya 21.7%/25 startups), and Nigeria 20.9%/24 startups).

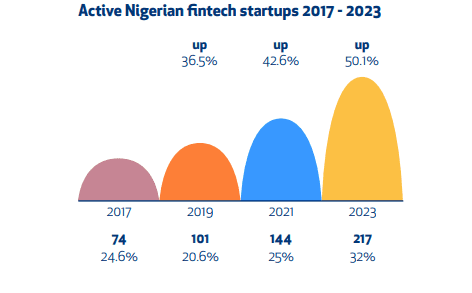

The report further stated that Nigeria had recorded major growth within two years. Within that period, the country surpassed South Africa to become the market with the most fintech startups. Nigeria’s fintech population has maintained regular growth. In 2017, it had 74. The number surged to 101 in 2019. Two years ago, there were 144 startups. There are 217 as of 2023, representing a 50.1% growth from 2021.

Read also: Moniepoint set to acquire Kenyan fintech Kopo Kopo Inc

Fintech remains a viable investment ground in the African tech ecosystem

Although the tech scene comprises diverse verticals like cleantech, healthtech, and proptech, fintech has played a major role in the ecosystem’s growth. Why is it irresistible? That’s because the sector houses startups striving to tackle a seemingly never-ending problem, financial inclusion.

An AFDB report defines financial inclusion as “all initiatives that make formal financial services Available, Accessible and Affordable to all segments of the population.” Virtually every fintech offers a solution they claim will close the gap between underserved communities and essential banking services. As such, it is a playing field with plenty to prove and lots of investors.

Speaking of investment, Nigeria’s economy may not be in the best shape today but fintechs in that market have managed to attract a huge volume of funding. Disrupt Africa’s study found that an astonishing $1.5 billion has been raised across 257 funding rounds since 2015. Not only is that a sizable amount, but it is the most any country on the continent has raised. It does not end there.

The report further stated that Nigeria’s funding for the past two years hit $1 billion. Meanwhile, Egypt-based fintechs also increased their stake in the African market by raising nearly $900 million in two years. Ghana also showed improvement as it generated over $100 million. Compared to the $3.5 million its startups secured in 2021, there’s a clear difference.