Africa’s tech scene keeps growing, and at the heart of this growth are two sectors leading the charge: fintech and e-commerce – the wizards of convenience, bringing banking and shopping to your fingertips.

But it’s not all smooth sailing. These companies face challenges, like rules and regulations and making sure everyone has internet access. Still, they keep pushing forward, finding new ways to grow and help people.

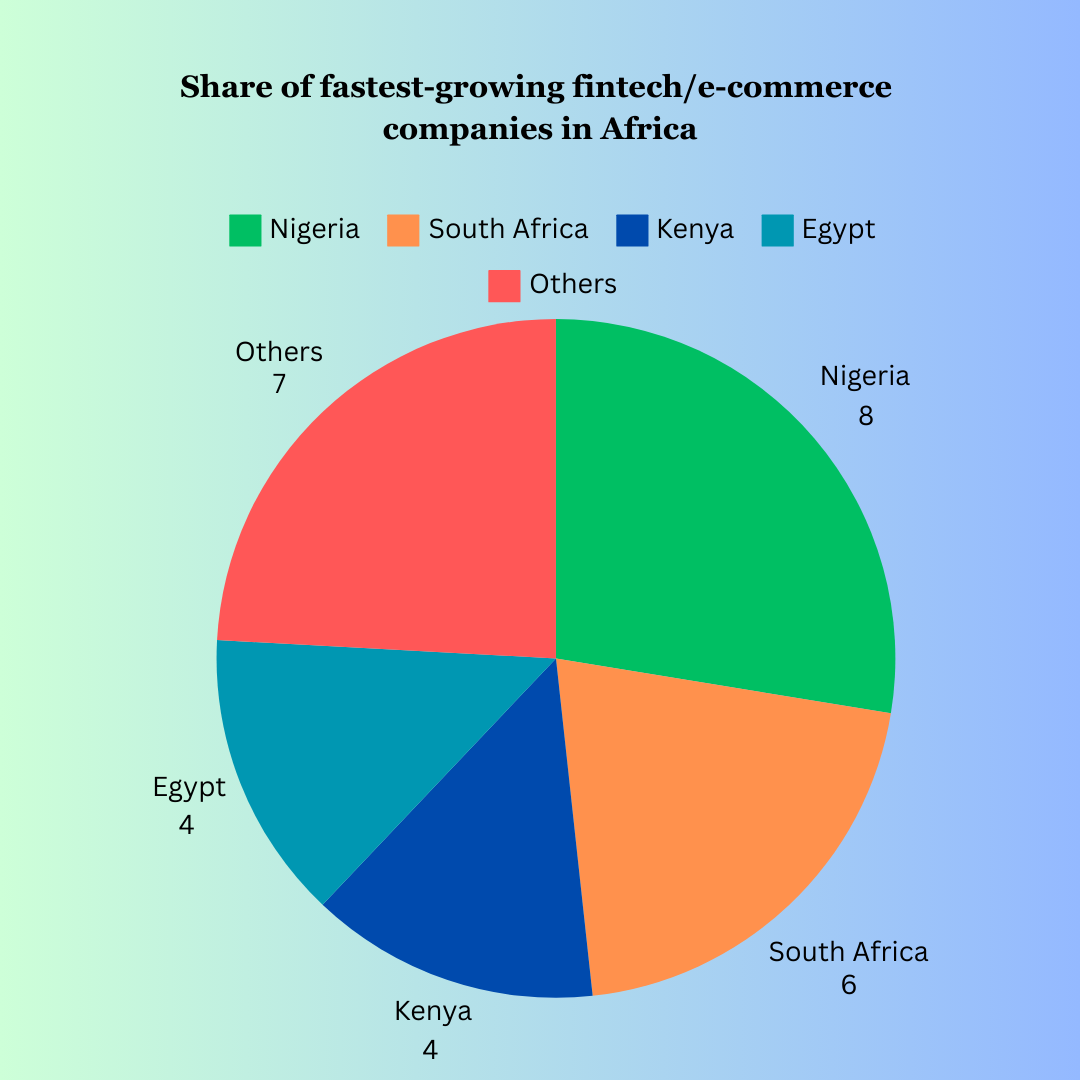

Criteria for inclusion in the list

To be included in the list of Africa’s fastest-growing companies, a company had to meet the following criteria:

- Revenue of at least US$100,000 generated in 2019 (1);

- Revenue of at least US$1.5mn generated in 2022 (1);

- An independent company (not a subsidiary or branch office of any kind);

- Headquartered in an African country (2);

- Revenue growth between 2019 and 2022 that was primarily organic (ie “internally” stimulated).

This article takes a closer look at Africa’s fastest-growing companies in fintech and e-commerce as listed by the Financial Times. It also considers the trends to understand, the factors driving these trends, the challenges and what it all means for investors, leaders, and everyday people.

Exploring Key Trends Shaping Growth

Several key trends are shaping their trajectory and redefining the continent’s economic landscape.

Fintech & Mobile Payment Revolution

In a 2022 article, McKinsey & Company says Africa has kept pace with the acceleration in the growth of human commerce — and in some cases even led — this innovation and an influx of new investments and regulatory shifts continues to shape the e-payments landscape on the continent.

Although cash is still king in Africa, a McKinsey survey suggests that its supremacy is likely to be challenged in the coming years as e-payments gain momentum.

“Africa leads the world in mobile money adoption, the primary driver of digital financial inclusion.” – Global Findex Database

This reinforces the fact that one of the most transformative trends in Africa’s financial sector is the widespread adoption of mobile payment solutions.

With the proliferation of smartphones and increasing internet connectivity, mobile wallets and payment apps have become commonplace, revolutionising the way people transact. From urban centres to remote villages – although this is questionable – individuals are embracing digital payments for everyday transactions, including bill payments, peer-to-peer transfers, and online purchases.

This trend not only fosters financial inclusion by providing access to banking services for the unbanked but also drives economic growth by facilitating commerce and trade.

The E-commerce Boom

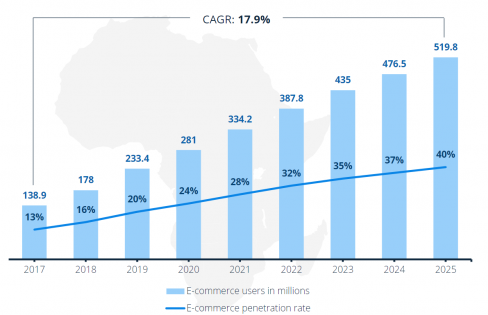

According to the International Trade Association, Africa is forecast to surpass half a billion e-commerce users by 2025, which will have shown a steady 17% compound annual growth rate (CAGR) of online consumers for the market.

E-commerce penetration to reach 40% by 2025.

The e-commerce sector in Africa is experiencing unprecedented growth, fuelled by a burgeoning middle class, rising consumer spending, and the proliferation of online marketplaces.

As more Africans gain access to the internet and become familiar with online shopping, e-commerce platforms are witnessing a surge in demand for a wide range of products and services. From fashion and electronics to groceries and household goods, consumers are embracing the convenience and accessibility of online shopping.

Moreover, the emergence of digital payment solutions and efficient logistics networks is facilitating the expansion of e-commerce across borders, enabling merchants to tap into regional and international markets.

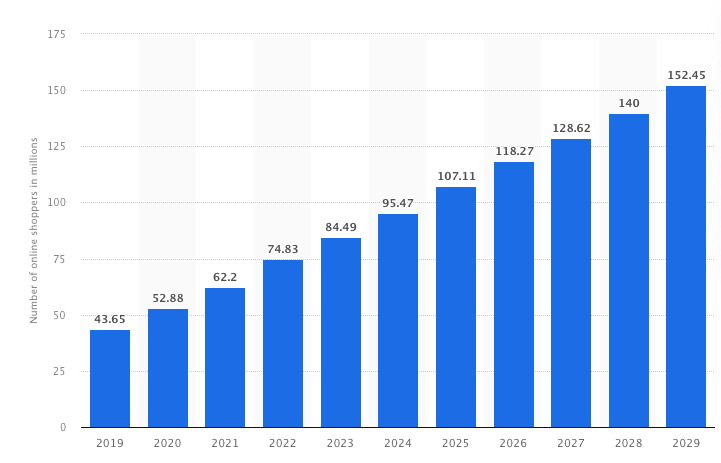

Statista paints a 10-year trajectory of e-commerce users as seen below:

Financial Inclusion Initiatives

Through innovative solutions such as mobile banking, microfinance, and digital lending, fintech startups are bridging the gap between financial institutions and unbanked populations, empowering individuals and small businesses to access credit, savings, and insurance services.

Fintech companies are playing a pivotal role in driving financial inclusion across Africa, particularly in underserved and rural areas where traditional banking infrastructure is limited. Kenya’s M-PESA mobile money system, for example, is famously purported to have lifted households out of poverty.

Also, the integration of alternative data sources and advanced analytics is enabling fintech companies to assess creditworthiness and mitigate risks, thereby expanding access to finance for previously underserved segments of the population.

A 2023 report from Boston Consulting Group (BCG), in collaboration with Elevandi “Driving Financial Inclusion in Africa”, highlights the growth of financial inclusion in Africa since M-PESA was founded in Kenya in 2007. While four countries (South Africa, Kenya, Uganda and Ghana) are growing financial inclusion above the regional average, fintech ecosystems in other African countries are maturing and attracting more investment.

Blockchain and Cryptocurrency Innovation

Notwithstanding the clampdown on crypto in countries like Nigeria, Africa is witnessing a surge in blockchain and cryptocurrency adoption, driven by the potential of these technologies to address various challenges in finance, governance, and identity verification.

From remittances and cross-border payments, blockchain solutions are being deployed to enhance transparency, efficiency, and security across diverse sectors.

Moreover, the growing interest in cryptocurrencies as alternative stores of value and investment assets is reshaping the financial landscape, with African entrepreneurs and investors exploring opportunities in digital assets and decentralised finance (DeFi).

Regulatory Dynamics

Regulatory frameworks play a crucial role in shaping the growth and development of fintech and e-commerce sectors in Africa.

While progressive regulations can foster innovation, protect consumers, and stimulate investment, regulatory uncertainty and inconsistency can impede industry growth and deter foreign investors.

Policymakers and regulators must strike a balance between promoting innovation and safeguarding the stability and integrity of financial markets.

Collaborative efforts between governments, regulators, industry players, and civil society are essential to create an enabling environment for fintech and e-commerce innovation while addressing regulatory challenges and ensuring compliance with international standards.

So, while immense opportunities are presented by the rapid growth of fintech and e-commerce in Africa, these industries also face a myriad of challenges that can hinder their development and impact.

Challenges

First, inadequate digital infrastructure and limited internet connectivity, especially in rural areas, hinder the widespread adoption of digital financial services and online shopping platforms. The lack (say absence) of a reliable power supply exacerbates these challenges, affecting operational efficiency.

Second, barriers to financial inclusion persist, with millions of unbanked and underbanked individuals facing hurdles such as lack of identification documents, limited access to digital devices, and low financial literacy levels.

Third, navigating the complex and fragmented regulatory environment poses significant challenges for startups and innovators. Unclear regulations and compliance burdens can stifle innovation and deter investment in these sectors.

Cybersecurity threats and data privacy risks also loom large as transactions move online. Cyberattacks and data breaches undermine consumer trust and expose sensitive financial information to exploitation by cybercriminals.

Also, the fragmentation of digital payment systems and interoperability issues hampers the seamless flow of transactions, leading to high costs and limited cross-border payment options.

Opportunities

The rapidly growing youth population across the continent presents a vast market for fintech and e-commerce solutions. With more young people embracing digital technology and smartphones, there is immense potential to tap into this demographic dividend and cater to their evolving needs and preferences.

Besides, the rise of mobile money and digital payments is revolutionising the way financial services are accessed and delivered in Africa.

Mobile money platforms such as M-Pesa in Kenya and MTN Mobile Money in Ghana are achieving widespread adoption, providing convenient and affordable financial services to millions of previously unbanked individuals. This trend opens up opportunities for innovative fintech startups to develop new products and services tailored to the needs of underserved populations.

Also, the growth of e-commerce platforms is reshaping the retail landscape in Africa, offering consumers greater convenience, choice, and affordability. With the increasing penetration of smartphones and internet connectivity, online shopping is becoming increasingly popular across the continent.

This presents opportunities for e-commerce startups to tap into this growing market and create innovative solutions to address the unique challenges of operating in Africa, such as last-mile delivery logistics and payment solutions.

We won’t forget the emergence of innovative fintech solutions such as peer-to-peer lending, digital lending platforms, and blockchain-based payment systems all democratising access to finance and empowering small businesses and entrepreneurs. These technologies have the potential to unlock new sources of capital and fuel economic growth and development across the continent.

The growing trend of cross-border eCommerce and international trade presents opportunities for African businesses to expand their reach and access new markets.

With the African Continental Free Trade Area (AfCFTA) poised to create the world’s largest single market, there is significant potential for e-commerce platforms to facilitate intra-African trade and drive economic integration and prosperity.

Implications for investors, policymakers and others

For investors, the burgeoning fintech and e-commerce sectors present compelling opportunities for capital deployment and portfolio diversification. But, funding has currently dropped over 40% in the past year, according to Africa: The Big Deal.

Investors must, however, understand that there is still immense potential to achieve attractive returns by backing high-growth companies that are disrupting traditional business models and capturing market share.

On their own, policymakers play a crucial role in fostering an enabling regulatory environment that supports the growth and sustainability of fintech and eCommerce ecosystems. By implementing policies that promote innovation, competition, and financial inclusion, governments can catalyse the development of vibrant digital economies that drive job creation, economic growth, and social development.

Policymakers need to address regulatory challenges such as data privacy, cybersecurity, and consumer protection to ensure the integrity and trustworthiness of digital financial services and eCommerce platforms.

For traditional financial institutions, the rise of fintech poses both opportunities and challenges. While fintech startups are disrupting traditional banking models and capturing market share, incumbents can leverage partnerships and collaborations with fintech firms to enhance their product offerings, improve operational efficiency, and reach new customer segments.

However, traditional banks must also adapt to the changing landscape by investing in digital transformation initiatives, upgrading legacy systems, and upskilling their workforce to remain competitive in the digital age.

The growth of eCommerce presents opportunities for traditional retailers to expand their reach and tap into new markets. By embracing digital platforms and adopting omnichannel retail strategies, brick-and-mortar retailers can enhance the customer experience, drive sales growth, and stay ahead of the competition.

Retailers must also address challenges such as logistics, supply chain management, and payment solutions to ensure seamless operations and customer satisfaction.

“The factors driving fintech investment in Africa should continue growing in the coming years,” said Mike David, founding partner at Olive Tree Ridge, a New York-based private equity firm. “The regulatory environment for fintech in Africa is still evolving, and there is a risk that new regulations could stifle innovation or create headwinds for startups to operate”, he also added.