The Central Bank of Nigeria (CBN) has recently lifted the restriction imposed on some fintech companies, including OPay, Kuda, Palmpay and Moniepoint, allowing them to resume onboarding new customers. This decision marks a significant shift in Nigeria’s digital banking regulatory landscape.

This order comes after the expiration of a May 31 deadline given to the fintech companies to meet specific compliance requirements. Here is a bit of background.

On April 29, 2024, the CBN issued a directive mandating fintech companies to halt the onboarding of new customers. This decision was a response to security concerns following the identification of 1,146 accounts engaged in peer-to-peer (P2P) cryptocurrency trading.

The primary aim was to curb activities that could potentially compromise the integrity of the financial system. The affected fintech companies including notable names like OPay, Moniepoint, Palmpay and Kuda, faced significant operational disruptions as they scrambled to meet the new regulatory requirements.

It is important to note that some fintech companies disputed the claim that the majority of implicated accounts belonged to their platforms.

The CBN’s crackdown was rooted in broader security and compliance issues, exacerbated by the rise of cryptocurrency transactions that often operate outside traditional regulatory frameworks.

The involvement of the country’s National Security Adviser (NSA) underscored the gravity of the situation, as cryptocurrency was classified as a security concern. This led to an intensified focus on Know Your Customer (KYC) protocols and fraud prevention measures, which were deemed essential to mitigate risks associated with digital financial transactions.

CBN’s requirements for lifting the ban

For the CBN to lift the restrictions on onboarding new customers, fintech companies must meet several stringent conditions to enhance security and compliance.

These requirements include:

- Physical address verification: All tiers of customer accounts now require physical address verification to ensure the legitimacy of account holders. This measure is intended to prevent fraudulent activities and improve customer data accuracy.

- Prohibition of P2P cryptocurrency transactions: Fintech companies have been mandated to block P2P cryptocurrency transfers to curb the risks associated with cryptocurrency trading. This step is crucial to addressing money laundering and illicit financial flows.

- Enhanced customer facial verification systems: Fintechs were also required to upgrade their facial verification systems. This technology is vital for confirming the identity of users and preventing unauthorised access to accounts.

These measures were designed to align fintech operations with the regulatory standards expected by the CBN, thereby fortifying the financial system against potential threats.

How it was before the ban

Before the ban imposed by the Central Bank of Nigeria (CBN), registering on fintech platforms like OPay and Palmpay was relatively straightforward and user-friendly. The process typically involved a few key steps designed to ensure ease of access while maintaining basic security protocols.

Here’s a general overview of how easy it was to register:

- Download the App:

- Create an Account: The registration process usually requires basic information such as name, phone number, and email address.

- Verification: Basic KYC (Know Your Customer) checks were performed, which might include verifying the phone number through an OTP (One-Time Password).

- Linking bank accounts: Users had the option to link their bank accounts or cards for seamless transactions.

- Minimal documentation: For lower-tier accounts, the documentation requirements were minimal, often not extending beyond a national ID or BVN (Bank Verification Number).

The process was designed to be quick, often taking just a few minutes to complete. But, while the registration process was easy, fintech platforms had implemented basic security measures to comply with regulatory standards:

– KYC procedures: Even before the ban, fintechs adhered to basic KYC protocols to verify the identity of users.

– Fraud prevention: Basic mechanisms were in place to detect and prevent fraudulent activities.

Reactions from the affected fintech companies

Some of the major players in the fintech community have responded well to the CBN’s decision to lift the restrictions, emphasising their commitment to compliance and customer security.

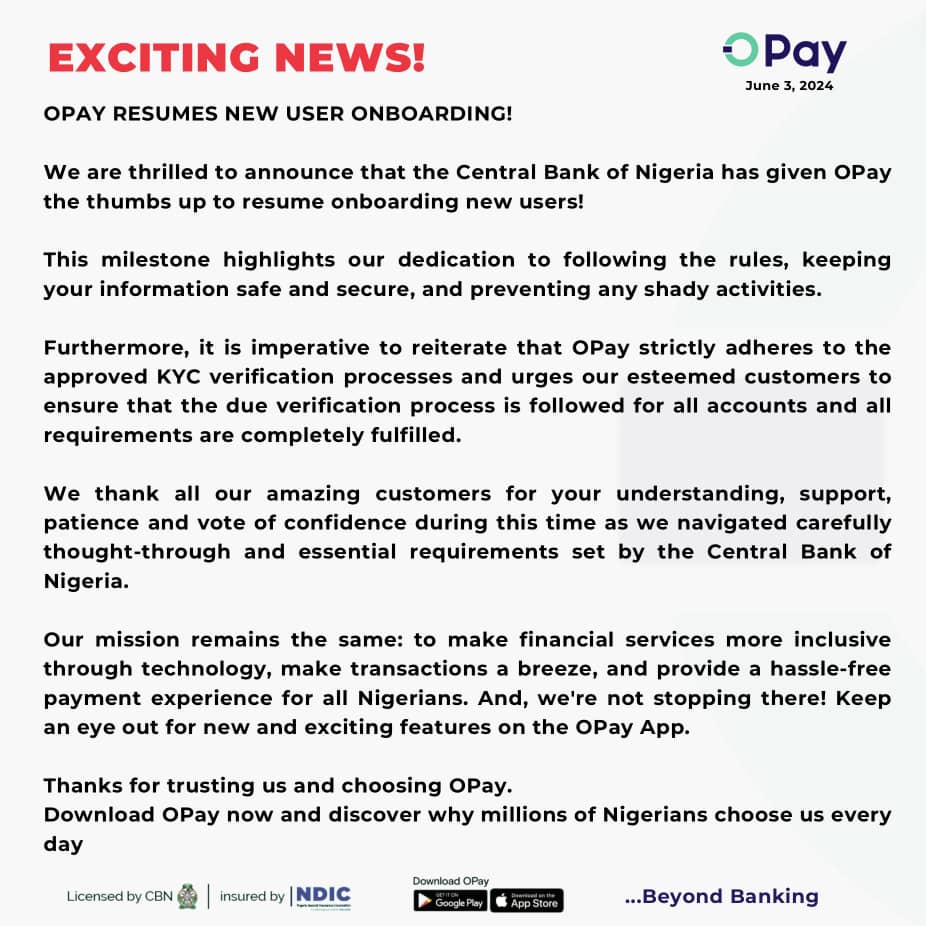

For instance, OPay took to its social media handle to express its excitement and reaffirm its dedication to adhering to the new regulatory requirements. OPay’s message to its customers highlighted its rigorous KYC verification processes and the importance of account verification.

Similarly, Kuda, another affected fintech company, announced the resumption of new customer sign-ups. In a statement shared on X, Kuda acknowledged the collaborative efforts with the CBN to implement necessary account controls and ensure regulatory compliance.

The company emphasised the need for customers to provide their Bank Verification Number (BVN), National Identification Number (NIN), and proof of address for opening Tier 3 accounts, indicating a robust verification process.

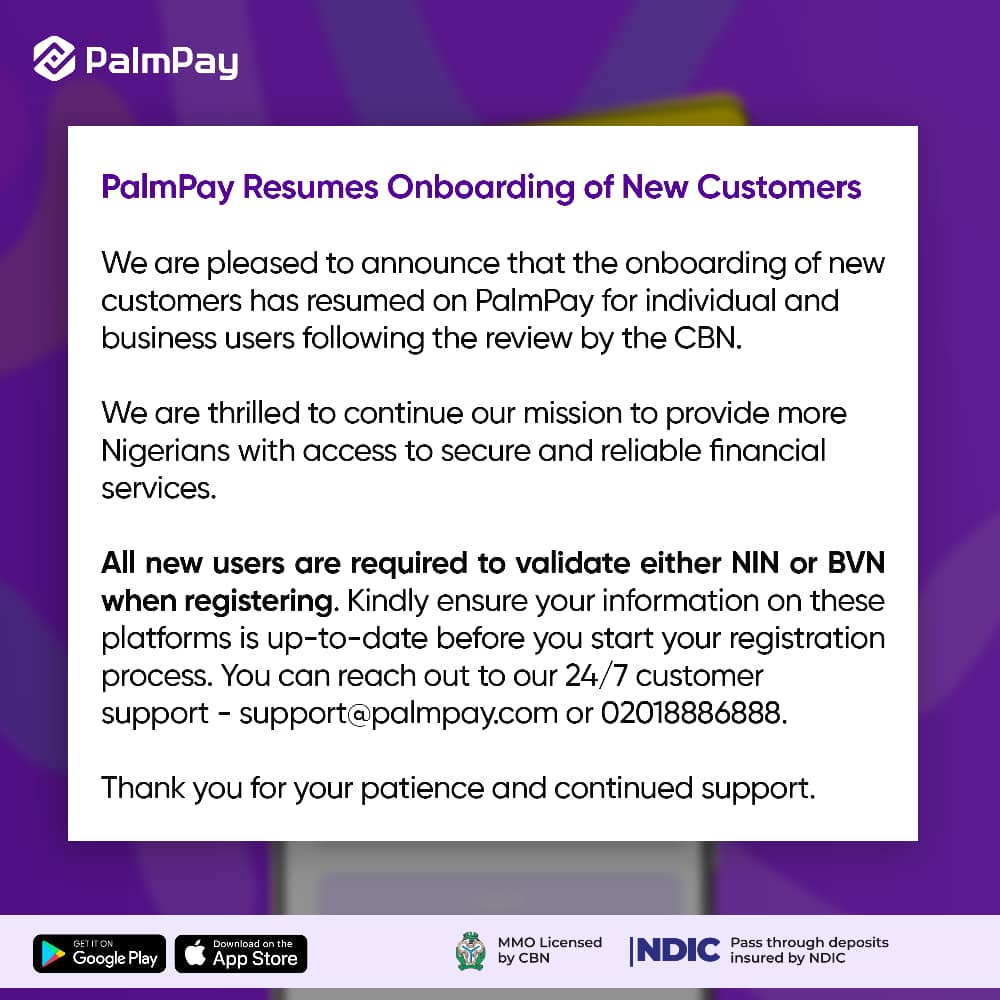

Palmpay wrote on X, “After regulatory review, we are back and ready to welcome you with open arms.”

Why this matters

“Regulation is very critical in a sector that seems to have grown so incredibly rapidly,” CBN governor, Olayemi Cardoso emphasised during the 295th Monetary Policy Committee meeting.

The decision by the CBN to lift the onboarding restrictions on fintech companies is crucial for several reasons.

First, it signifies a renewed trust in the fintech sector’s ability to comply with regulatory standards. By meeting the stringent requirements set by the CBN, these companies have demonstrated their commitment to maintaining high levels of security and transparency.

Second, this move is essential for the growth and development of the fintech industry in Nigeria. Fintech companies play a pivotal role in driving financial inclusion, offering innovative solutions that cater to the unbanked and underbanked populations.

Besides, CBN’s decision underscores the importance of regulatory oversight in the rapidly evolving fintech landscape.

As highlighted by Cardoso, the measures put in place aim to curb money laundering and illicit financial flows, ensuring that the fintech sector operates within a robust regulatory framework. This enhanced regulatory environment is expected to build customer trust and confidence, which is vital for the long-term sustainability of digital financial services.

Future implications

Looking ahead, the lifting of the onboarding restrictions is likely to have several positive implications for the fintech sector in Nigeria.

Firstly, fintech companies can now focus on expanding their customer base, driving innovation, and enhancing their service offerings. This growth is expected to contribute to increased competition within the financial services industry, ultimately benefiting consumers through better products and services.

Also, the strengthened regulatory framework will serve as a foundation for future developments in the fintech space. With heightened surveillance and compliance measures in place, the sector is better equipped to prevent fraud and other illicit activities, like the one with Nigerian actress, Shan George who shared a video on her Instagram account appealing for help to recover her money, saying, “Cecilia Chiagoziem Okoro that is the name of the person that have just wiped all the money in my account, 3.6 million [naira] into an Opay account.”

The new KYC requirements not only protect consumers but also enhance the overall stability and integrity of the financial system.

The collaboration between the CBN and fintech companies sets a precedent for constructive engagement between regulators and industry players. This assumed cooperative approach is essential for addressing emerging challenges and opportunities in the fintech sector, ensuring that regulatory policies keep pace with technological advancements.