Every other week, it feels like there’s a new remittance startup launching in Nigeria. Each one promises faster transfers, lower fees, or better rates. But if we’re being honest, how many of them are solving the real problems users face?

Nigeria’s remittance inflows are projected to reach $26 billion by 2025, up from $20.1 billion in 2021. This surge is fuelled by the ‘Japa’ wave, the mass emigration of Nigerians seeking better opportunities abroad. Consequently, the remittance sector has become a magnet for fintech innovation.

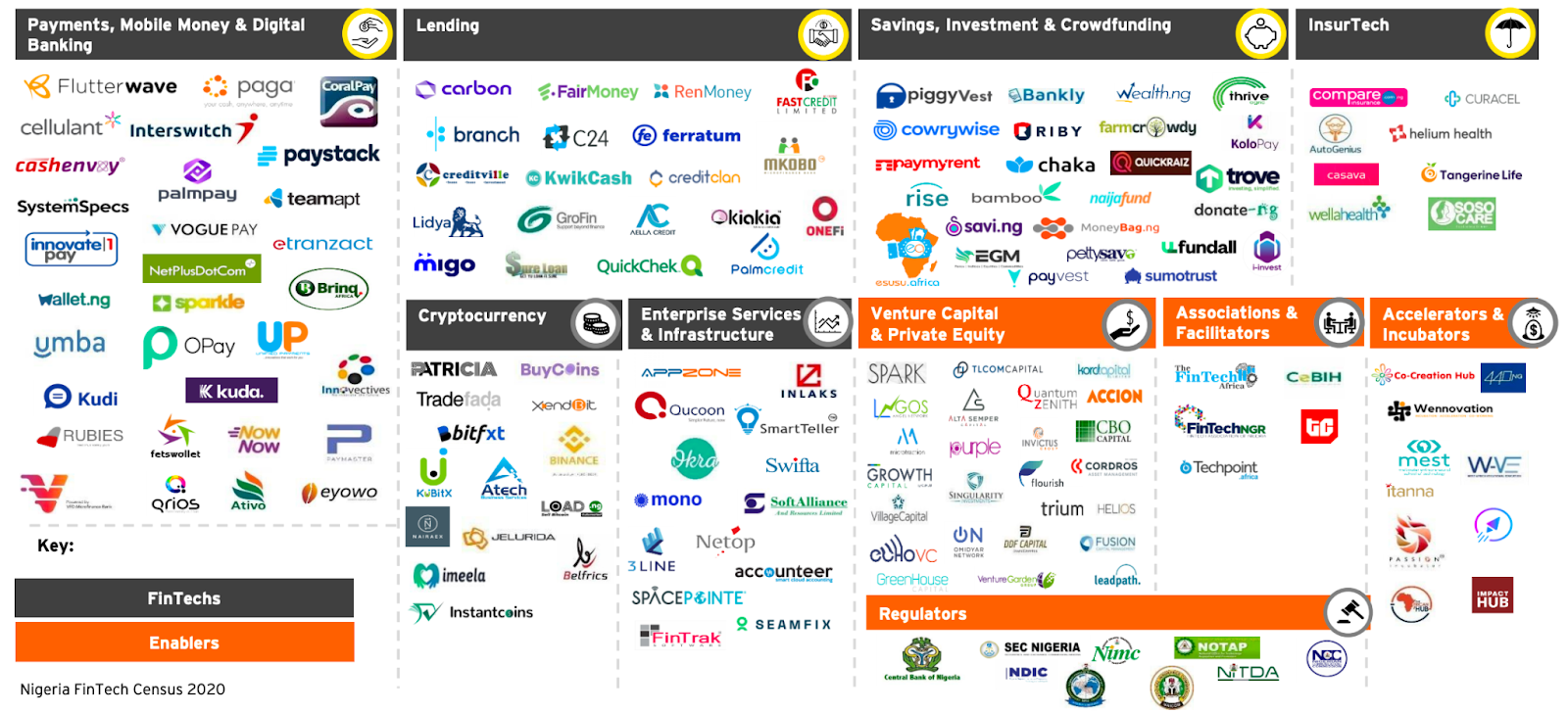

Payment and remittance firms now dominate Nigeria’s fintech landscape, accounting for over 30% of the market share. With the number of fintech startups in Nigeria increasing by over 50% from 144 in 2022 to 217 in 2023, the competition is intensifying.

The 2025 edition of the Nigeria Fintech Map says Nigeria was home to more than 430 fintech companies as of February 2025, marking a remarkable increase from the 255 companies mapped in January 2024.

The report categorises these companies into 12 verticals, with the largest being business payments and cross-border transactions, credit infrastructure and digital lending, and spend management, buy now, pay later (BNPL) and merchant solutions, with 56, 54, and 53 companies, respectively.

Despite this proliferation, the digital remittances market in Nigeria is still maturing. Statista projects the transaction value in this market to reach $46.70 million in 2025, with an average transaction value per user of $900. This indicates significant room for growth and innovation.

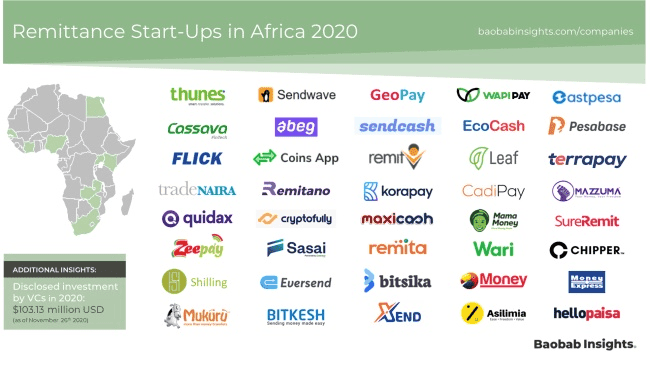

We compiled a list of some of the most prominent remittance startups, what makes them different (or not), and how widely adopted they are. Because maybe the issue isn’t that we have too many remittance startups—it’s that too many of them are doing the same thing.

With so many players entering the space, it’s easy to lose track. So, we decided to take a step back and break it down. What exactly do these platforms offer? Who are they targeting? And, most importantly, how many people are using them?

Remittance startups serving Nigerians :

| Startup | Year Launched | Top Corridors | Unique Features / USP | Estimated Users |

| LemFi | 2021 | UK, US, Canada → Nigeria | Multi-currency wallets; over 30 supported countries; $1B+ monthly transfers | 1M+ users |

| Send App (Flutterwave) | 2021 | US, UK, Canada → Nigeria, Ghana, Kenya | Built on Flutterwave’s infrastructure, supports 30+ countries, fast transfers | Not publicly disclosed |

| Payday (integrated into Changera) | 2021 | Global → Nigeria | Virtual USD/GBP/EUR accounts; instant currency swaps; virtual cards | Not publicly disclosed |

| Grey | 2021 | US, UK, EU → Nigeria, Kenya, Tanzania | Foreign bank accounts for freelancers; instant FX conversion | Not publicly disclosed |

| Kyshi | 2020 | UK, US → Nigeria, Ghana | Peer-to-peer FX marketplace; user-driven rates | Not publicly disclosed |

| WeWire | 2022 | Global → Africa | B2B cross-border payments across 80+ countries; multi-currency support | Not publicly disclosed |

| finREMIT | 2023 | UK → Nigeria | SME-focused remittances; aims to channel £200K in Q1 2024 | New entrant |

| Wirepay | 2020 | Nigeria, Ghana, Kenya | Multi-currency wallets (USD, NGN, GHS, KES, XAF); virtual USD cards; currency exchange without intermediaries; fast and secure transfers via mobile money, bank transfers, cash pickups, or Wirebeam | Over 50,000 users (as of October 2022) |

| Eversend | 2017 | Nigeria, Ghana, Kenya, Rwanda, Uganda, Cameroon, Zambia | Multi-currency wallets (USD, EUR, GBP, NGN, GHS, KES, RWF, UGX); virtual USD cards; wallet-to-wallet transfers; mobile money and bank transfers; bill payments; airtime purchases | Over 500,000 users (as of July 2022, according to Google Play) |

| Monirates | 2022 | Nigeria, Ghana, Kenya, Uganda, Benin, Togo, Ivory Coast, Cameroon, Malawi | Multi-currency support (NGN, GHS, KES, UGX, XOF, XAF, GBP); intra-African transfers; tuition payments; business transactions; low fees (<1%); decentralised payment network | Not publicly disclosed |

While user numbers for many of these startups (including Pexbank, Passportmonie, CREDEQUiTY, Scalex Protocol, Bingtellar) are not publicly disclosed, LemFi stands out with over 1 million users and significant transaction volumes.

The diversity in features—from multi-currency wallets to peer-to-peer FX marketplaces—highlights the innovative approaches these startups are taking to address remittance challenges.

You can argue that the Nigerian remittance landscape is experiencing a significant transformation, with startups rapidly emerging to address the growing demand for cross-border financial services. This surge is driven by the increasing need for efficient, affordable, and accessible remittance solutions for Nigerians both at home and abroad.

Correlating user numbers with innovation

The correlation between user numbers and innovation is evident in the Nigerian remittance sector.

In a 2016 report for BusinessDay, Daniel Obi writes:

“Remittances have a distributive impact on households as income and consumption patterns are affected. The vast majority of remittances are used to provide for the basic needs of households, regardless of the country, with siblings and parents the most likely recipients.

“Generally, the major uses of remittances in Nigeria include housing, consumption, and education financing, with spikes generally observed in remittance flows during back-to-school and pre-Christmas periods.”

Therefore, startups that offer unique solutions tailored to the specific needs of Nigerians are witnessing substantial user adoption. For instance, LemFi’s focus on simplifying cross-border transactions has resonated with a broad user base, leading to its impressive growth metrics.

Conversely, newer entrants like Monirates are carving out niches by addressing specific challenges in the remittance process, such as offering peer-to-peer currency exchange at user-preferred rates. While their user bases may currently be smaller, their innovative approaches have the potential to disrupt traditional remittance models and attract a dedicated user segment.

Is the problem being solved?

High fees

Despite the proliferation of remittance startups, transaction costs remain a significant hurdle. In rural Nigeria, for instance, residents often pay fees ranging from 1% to 2% per transaction when using Point of Sale (POS) agents.

For low-income earners, these fees are prohibitive, leading many to revert to informal channels for money transfers. This not only undermines the digital payment ecosystem but also exacerbates financial exclusion.

Besides, some fintech entities have been known to charge up to 10% of the transaction value, further discouraging the use of formal remittance channels.

???? FX Transparency

The unification of Nigeria’s exchange rate regime in 2023 aimed to enhance transparency in FX transactions. However, challenges persist.

Fintech platforms often offer exchange rates that are not communicated to users, leading to mistrust and reluctance to use these platforms. Also, the competition between banks and fintech platforms has intensified, with both offering varying rates and services, making it difficult for consumers to make informed choices.

Bridging the divide

Access to remittance services in both rural and urban areas remains limited. At the start of 2025, 107 million Nigerians had internet access, representing a 45.4% online penetration rate, leaving over 50% in the dark.

This digital divide hampers the widespread adoption of fintech solutions in rural communities. And, sometimes, residents often have to travel long distances to access financial services, incurring additional costs.

Technical glitches and data management issues

Users frequently encounter technical issues such as transaction failures, disappearing funds, and outdated account details.

These problems are often attributed to poor data management practices, including duplicate records and unreliable analytics, which delay dispute resolution and erode customer trust in digital payment systems.

Complex user interfaces

The design of many fintech applications lacks user-centric considerations, leading to confusing navigation and transaction processes. Users have reported experiences akin to “solving a puzzle” when attempting to send money, highlighting the need for more intuitive and accessible interfaces.

Differentiation vs. Duplication

Many remittance startups in Nigeria offer similar services—fast transfers, low fees, and user-friendly apps. This lack of differentiation leads to market saturation and price wars, eroding profit margin. Without unique value propositions, startups struggle to retain customers and achieve sustainable growth.

To illustrate, payment and remittance firms dominate Nigeria’s fintech sector, holding over 30% of the market share, as reported by Agpaytech. This concentration indicates a crowded market where numerous players vie for the same customer base with comparable offerings.

To stand out, some fintech entities are bundling additional services such as bill payments, savings, and lending. However, these efforts are still in nascent stages, and widespread adoption remains limited.

More startups, same solutions?

The expansion of the fintech space in Nigeria has led to concerns about market saturation and a lack of differentiation among services.

The CEO of Aladdin Digital, Darlington Onyeagoro, said in 2023:

“Where we are today, the fintech space in Nigeria is almost saturated. There are so many players. For loan apps alone, the last time I checked, there are over 300 or 400 lending companies via apps on the Play Store. That is the Play Store alone, I’m not talking about IoS.”

Onyeagoro describes the current state as a “red ocean,” where many players offer similar solutions, making it challenging for newcomers to gain visibility without significant funding or truly disruptive ideas. Despite the proliferation of services, core issues such as high transaction fees, limited FX transparency, and inadequate rural access persist.

Besides, the underlying infrastructure supporting these fintech solutions remains fragile. Many companies rely on foreign technologies for essential services like payment gateways and fraud detection, leading to increased operational costs and scalability challenges. This reliance hampers the ability of fintech platforms to provide consistent and accessible services, particularly in underserved regions.

But, on a conclusive note, maybe we don’t need fewer startups. Maybe we need better focus.