Nigeria’s Point-of-Sale (POS) terminals recorded ₦18.32 trillion across 1.38 billion transactions in 2024, largely attributed to the country’s fintech industry.

This was revealed in “The State of Enterprise 2025 Report” by EnterpriseNGR, which provides an in-depth analysis of Nigeria’s Financial and Professional Services (FPS) Sector, described as an engine of innovation, opportunity, and growth.

According to the report, Nigerian fintech’s contribution to financial inclusion is labelled to have provided millions of Nigerians with financial access without visiting bank branches.

The innovative features provided by these platforms boosted financial resilience by leveraging digital solutions that enable millions to save, invest, borrow, and transact with ease.

As a testament to the rise in card-based and mobile retail payments, mobile money operators facilitated ₦79.55 trillion in transactions, a 70.6% increase from 2023, where transaction volumes grew by 28%, from 3.04 billion to 3.9 billion.

Fintech platforms raised the use of electronic channels for transactions with e-bill payments of ₦2.1 trillion across 300,000 transactions, while ‘Mobile Pay’ witnessed ₦75.55 trillion across 3.9 billion transactions.

Nigerian fintech entities also boosted remittance inflows and enabled widespread adoption of mobile-first financial platforms. Through this, NIBSS instant payment transactions reached ₦1.07 quadrillion, representing an 80% increase from ₦600.36 trillion recorded in 2023. Explicitly, December 2024 alone saw ₦115.1 trillion in transactions, up from ₦71.9 trillion in December 2023.

Also Read: Moniepoint, Flutterwave listed in Time100 2025 companies list.

Digital payment’s growth

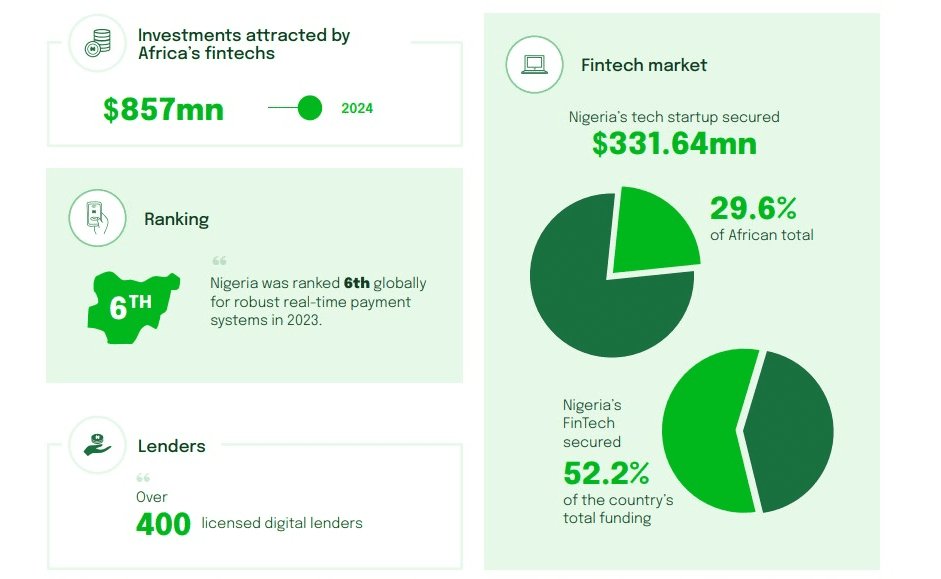

Nigeria’s fintech startups secured a total funding of $331.64 million in 2024, representing 52.2% of Nigeria’s total funding in 2024. According to the report, Nigeria’s fintech sector has played a pivotal role by providing digital platforms that improve access to capital and operational efficiency for businesses.

“The Nigerian fintech sector experienced growth across diverse verticals, from blockchain adoption to increasing cryptocurrency usage and widespread digital payments. Regulatory developments kept pace, with 2024 witnessing the introduction of several targeted laws, regulations, and circulars covering remittances, cryptocurrencies, foreign exchange, and more,” the report noted.

The sector had a significant impact on the country’s economy, with key contributions across digital payments, automating billing and payroll, and the Buy Now, Pay Later (BNPL) customer service offering.

Between 2021 and 2024, the BNPL service grew at a 23.1% compound annual growth rate (CAGR) and is projected to grow from $1.42 billion in 2024 to $2.61 billion by 2030.

With more than 400 licenced digital lenders across Nigeria, fintech loan apps have advanced financial inclusion by providing affordable credit to underserved individuals and SMEs with limited financial history or collateral.

As stated in the report, the integration has strengthened remittance services as increased competition boosted inflows by 63.7%, from $2.33 billion in 2023 to $3.82 billion in 2024.

Nigeria also saw notable expansion of innovation hubs, which extended beyond major cities like Lagos, Abuja, and Port Harcourt to smaller areas such as Ilorin, signifying that Nigeria’s tech ecosystem is expanding rapidly. With an estimated growth of $32.8 billion in 2025, Nigeria’s ICT market is projected to grow at a CAGR of 18.3% from 2025 to 2030 to reinforce its role as a key player in Africa’s digital economy.

With 5 unicorns – Moniepoint, OPay, Paystack, Interswitch, and Flutterwave (out of Africa’s 8), Nigeria’s fintech is poised for a global revolution. The country was ranked 6th globally for a robust real-time digital payment system in 2023.

Nigerian fintech leading Africa’s transformation

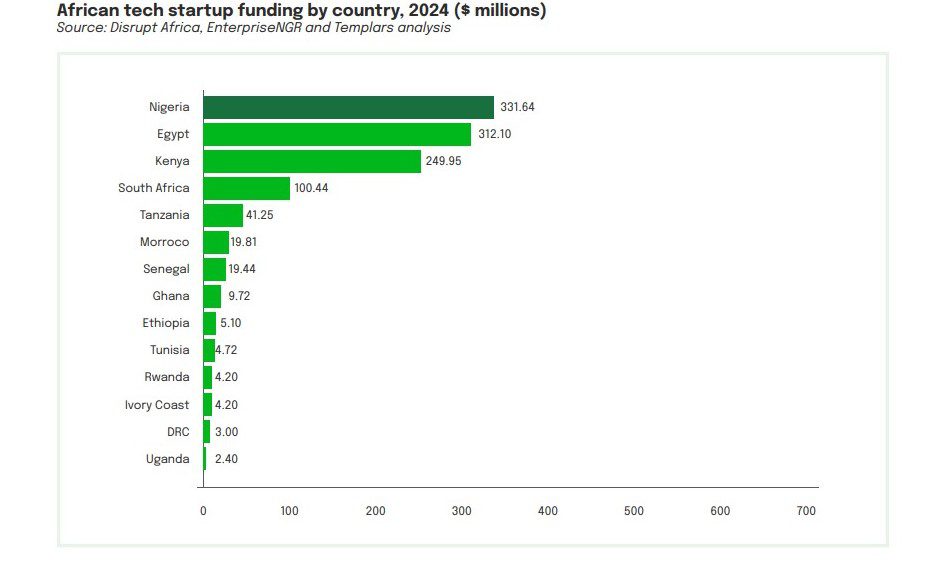

The continent witnessed a sharp decline in tech startups’ funding by 53.5% to $1.12 billion (down from a record $2.41 billion in 2023), but Nigerian fintech firms attracted the highest funding value on the continent by securing $331.64 million, representing 29.6% of Africa’s total.

The funding was distributed among 39 Nigerian startups (19.5% of all funded startups), placing Nigeria second only to Egypt, which had 51 funded startups securing $312.10 million. Others in the top ten are Kenya ($249.95 million), South Africa ($100.44 million), Tanzania ($41.25 million), Morocco ($19.81 million), Senegal ($19.44 million), Ghana ($9.72 million), Ethiopia ($5.10 million) and Tunisia ($4.72 million).

Notably, around 40% of Nigeria’s funded startups operated in the fintech sector, securing 52.2% of the country’s total funding.

Challenges and way forward

Amid its successes and significant contributions, Nigeria’s fintech sector faces several challenges that hinder the realisation of its full actualisation, such as government regulations, foreign exchange rates, the digital divide, and financial penetration into rural areas.

Since post-COVID, reports revealed that startup funding dropped by 172% from about $900 million in 2022 to $331.64 million in 2024, while the number of Nigerian fintech entities that secured funding dropped by 361.5% to 39 from 180.

To mitigate future negative impacts, the reports encouraged substantial investment in cybersecurity infrastructure, firewalls, encryption, and intrusion detection systems.

While inconsistent internet connectivity in many parts of the country continues to restrict the adoption of digital financial services in underserved areas, fintech companies are encouraged to focus on developing offline-capable applications that work with low connectivity.

Also, the adoption of regulatory sandboxes by both the Central Bank of Nigeria (CBN) and the Securities and Exchange Commission (SEC) is tagged as a digital innovation tool that can fully support Fintech innovation.

The report encouraged “moving from a cohort-based sandbox approach to an open-ended approach and building trust in the use of sandboxes” to increase adoption.