Global personal computer (PC) shipments maintained robust growth in the second quarter of 2025, signalling proactive moves by vendors to navigate looming tariff deadlines, according to a new report from International Data Corporation (IDC).

The IDC Worldwide Quarterly Personal Computing Device Tracker, released on July 21, 2025, highlights a 3.1% year-over-year increase in global PC shipments, totalling 64.9 million units. This marks the third consecutive quarter of growth, driven by strategic inventory stocking and strong demand in key markets.

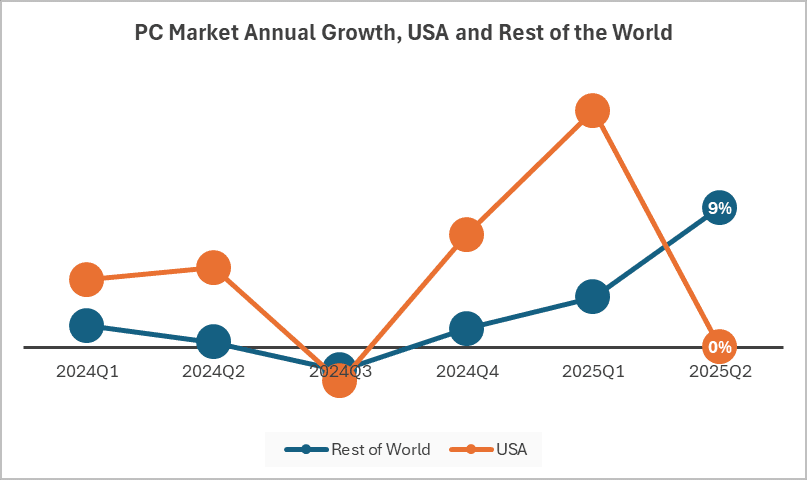

The PC market’s resilience is recorded despite challenges like economic uncertainty and geopolitical tensions. IDC notes that vendors are accelerating shipments to preempt potential tariff hikes, particularly in the United States, where trade policies could impact costs.

“Vendors are getting ahead of potential disruptions,” said Ryan Reith, group vice president at IDC’s Mobility and Consumer Device Trackers. “This proactive approach has helped sustain shipment volumes, especially in the commercial and education sectors.”

The report points to a recovery from the post-pandemic slump, with 2025 shaping up as a pivotal year for the PC industry. Growth in commercial deployments, particularly in enterprises upgrading to Windows 11, has been a key driver. Education sectors also contributed, with schools refreshing devices for hybrid learning environments. However, consumer demand remains uneven, with budget-conscious buyers favouring entry-level devices.

Global PC regional and vendor highlights

The United States saw particularly strong performance, with shipments up 4.2% year-over-year, fuelled by enterprise upgrades and tariff-related inventory builds. Asia/Pacific (excluding Japan) also posted gains, driven by demand in China, where Huawei reclaimed the top spot in the smartphone market but also bolstered its PC presence.

Among vendors, Lenovo maintained its lead with a 22.7% market share, shipping 14.7 million units, a 2.8% increase from Q2 2024. HP Inc. followed with 13.7 million units and a 21.1% share, benefiting from strong commercial demand. Dell Technologies held steady in third place, shipping 10.1 million units, while Apple’s Mac shipments grew 4.9%, driven by refreshed MacBook models. ASUS rounded out the top five, capitalising on gaming and premium device demand.

“Lenovo’s focus on diversified portfolios, from budget Chromebooks to high-end workstations, has kept it ahead,” said Jitesh Ubrani, research manager at IDC. “Meanwhile, Apple’s growth reflects its ability to capture premium buyers.”

The spectre of tariffs has loomed large over the PC industry. With potential trade restrictions on the horizon, vendors have ramped up production and shipments to stockpile inventory in key markets.

This strategy mirrors trends seen in other tech sectors, such as smartphones, where manufacturers are also preparing for supply chain disruptions. IDC analysts warn that while this approach has bolstered Q2 figures, it could lead to oversupply if demand softens in Q3.

“Vendors are walking a tightrope,” Reith noted. “They are balancing the need to maintain inventory with the risk of overstocking if consumer spending slows.”

The report suggests that promotional activity, such as back-to-school sales, will be critical to sustaining momentum through the second half of 2025.

The IDC report underscores a shift in market dynamics. While traditional PCs, desktops, notebooks, and workstations accounted for the bulk of shipments, Chromebooks saw a notable resurgence, particularly in education. Shipments of Chromebooks grew 7.4% year-over-year, driven by affordability and cloud-based functionality. Conversely, gaming PCs maintained steady demand, with ASUS and Lenovo capitalising on enthusiast markets.

Meanwhile, IDC has projected moderate growth for 2025, with global PC shipments expected to reach 260 million units, a 2.5% increase from 2024. However, uncertainties around inflation, consumer confidence, and trade policies could temper this outlook.

“The industry is at a crossroads,” said Ubrani. “Sustained growth will depend on innovation, competitive pricing, and navigating geopolitical headwinds.”