Start with a number the Nigerian government would rather not display in public. Six per cent. That is the share of 26,000 Nigerians who, when asked by PiggyVest how they feel about their overall financial situation in 2025, say they feel secure and content.

The remaining 94% describe some form of financial strain, from the 31% who say they often feel stressed or constrained by their finances, to the 29% who describe their current financial situation as one they are extremely unhappy with.

Another 22% report feeling neither satisfied nor dissatisfied, floating in a neutral space that offers no real cushion.

The figure comes from the PiggyVest Savings Report 2025, a survey of over 26,000 Nigerians across all six geopolitical zones conducted between August and September 2025. It is the most expansive consumer financial health survey in Nigeria, and the number it puts on financial security is one of the starkest indictments of the gap between macroeconomic progress and lived experience to emerge from Nigerian data this year.

The macroeconomic story Nigeria’s government tells sounds reasonable on the surface.

The World Bank’s October 2025 Nigeria Development Update recorded GDP growth of 3.9% year-on-year in the first half of 2025. The IMF noted that inflation fell from a 31% annual average in 2024 to 23.7% year-on-year by April 2025, driven by naira stabilisation and improvements in food supply.

Foreign reserves crossed $42 billion. Public debt declined for the first time in over a decade.

Read also: Piggyvest: Rent, vacation, new business dominate users’ savings target in 2025

None of that shows up in the 6%.

The PiggyVest report does not leave the number without context. Its researchers went further and examined who, exactly, compose that 6%. The finding overturns a basic assumption about wealth and wellbeing.

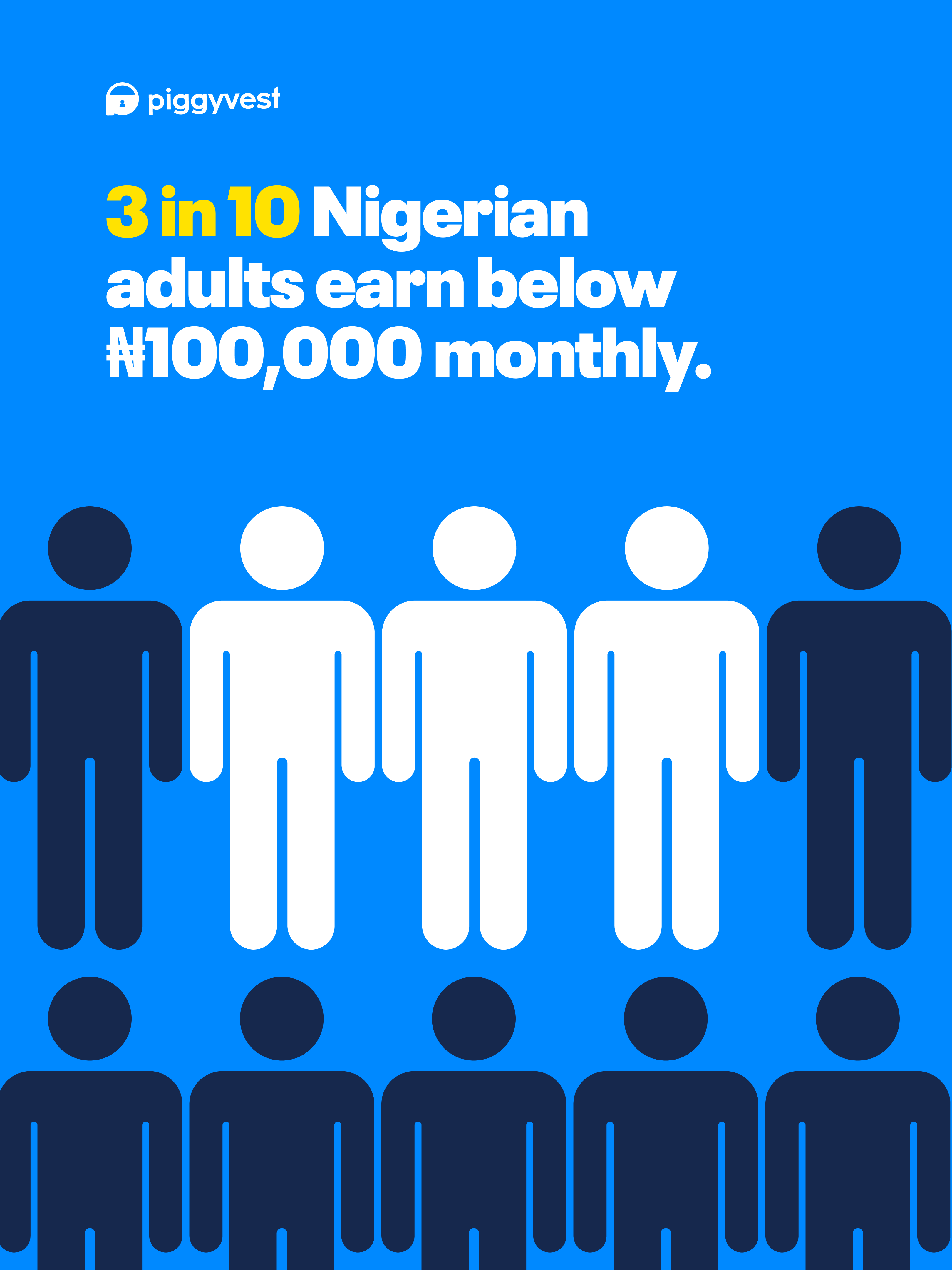

Respondents who feel financially secure are found across all income levels, but the majority fall within low-to-middle income brackets rather than the highest bands. Only 12% of those who describe themselves as financially secure and content earn ₦5 million or more per month.

Meanwhile, 14% of the financially secure group earns below ₦100,000, and 21% earns between ₦100,000 and ₦249,999. A further 10% currently has no monthly income at all.

Read that again. One in ten Nigerians who say they feel financially secure reports having no monthly income.

This is the finding that should reshape how policymakers and financial institutions talk about financial wellbeing in Nigeria. Higher income does not automatically guarantee satisfaction. Something else is doing the work.

The report points to consistent saving habits and fewer obligations as the more likely drivers. Among those who feel financially secure, 54% save a fixed portion of their income every month. The report calls this the strongest single predictor of perceived financial stability. In contrast, among the broader population, only 40% save monthly, and that figure has been falling for three consecutive years.

EFInA’s own research is direct on this point: only 16% of Nigerian adults were financially healthy in 2023, down from 28% in 2020. In 2023 alone, 84% of adults ran out of money at least once, 58% sometimes went without food, and 78% could not raise emergency funds within a week. That data was collected before the full weight of 2024’s 34.8% peak inflation landed on household budgets.

The PiggyVest report’s financial satisfaction chapter adds the emotional layer those figures lack. When respondents are asked directly about their progress toward major financial goals, homeownership, education, business, only 7% say they feel confident and ahead. More than 1 in 3, 36%, say they feel far behind or stuck. A further 17% describe their trajectory as unpredictable, some days on track, other days completely hopeless.

The sources of that anxiety are not what casual observers might assume. When the report asks respondents about the most stressful financial decision made in the past six months, only 6% cite a large discretionary purchase such as an appliance or phone.

The real pressure points are structural and recurring: rent and housing at 14%, financial support for family or friends at 14%, school fees at 13%, and starting a business at 13%. Together, these four categories account for more than half of all reported financial stress.

The World Bank’s October 2025 Nigeria Development Update confirmed the stakes on housing costs, noting that poor households spend up to 70% of their income on food, with the cost of a basic food basket rising fivefold between 2019 and 2024.

More than 1 in 2 Nigerians enters each month unsure whether their income will cover basic expenses.

That statistic appears in the PiggyVest report as a summary finding, and it sits uncomfortably alongside the IMF’s April 2025 assessment, which praised Nigeria’s macroeconomic reforms and projected continued disinflation in the medium term. The reforms are real. The stability they promise has not arrived at the household level.

What the 6% figure ultimately tells us is that financial security in Nigeria is a behavioural and structural achievement, not an income milestone.

The Nigerians who have it tend to save regularly, carry lighter family obligations, and operate with greater cashflow predictability. They exist at every income level. The majority of Nigerians who do not have it are not simply poor. They are unstable, carrying obligations that leave no room to build buffers, in an environment where every month brings a fresh test of how much strain a household can absorb before something breaks.