Across Nigeria’s five biggest commercial banks, a decade-long leadership cycle is closing. The Central Bank’s 12-year tenure rule has arrived. But the men stepping out of formal roles are buying more shares, not fewer.

On an unremarkable Tuesday, Jim Ovia stepped down as chairman of Zenith Bank. There was no crisis, no market reaction (except a 0.93% drop as of the time of reporting), no statement of regret from the board.

Just the expiry of a regulatory clock that the Central Bank of Nigeria (CBN) had set years ago, and which had been ticking quietly ever since.

The CBN limits tenure for bank chairmen and key executives to 12 years. Ovia had reached the ceiling. The exit was orderly, compliant, and predictable to anyone who had been tracking the governance timelines of Nigeria’s biggest banks.

What was not predictable, at least not from the outside, was what Ovia did while the clock ran down.

He bought more shares.

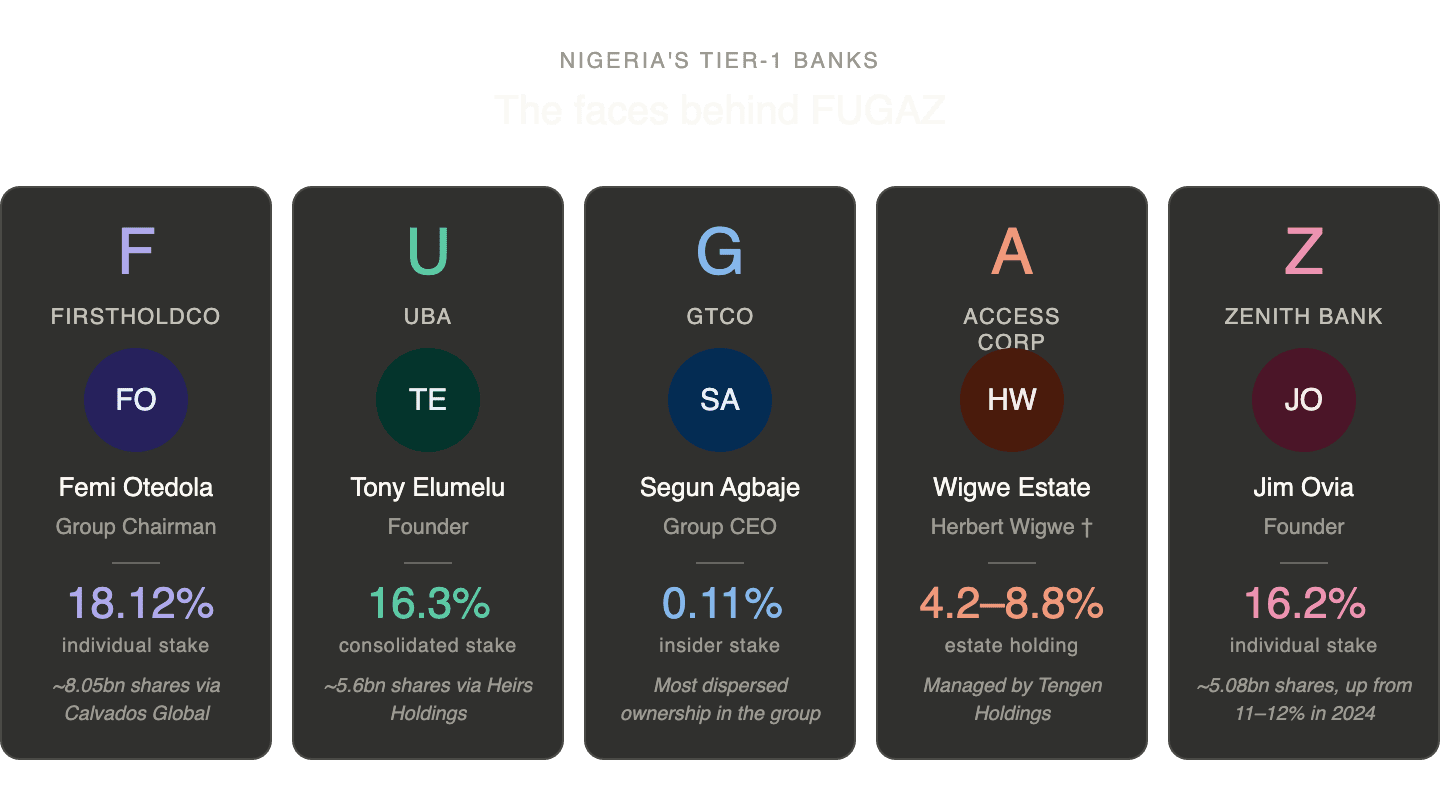

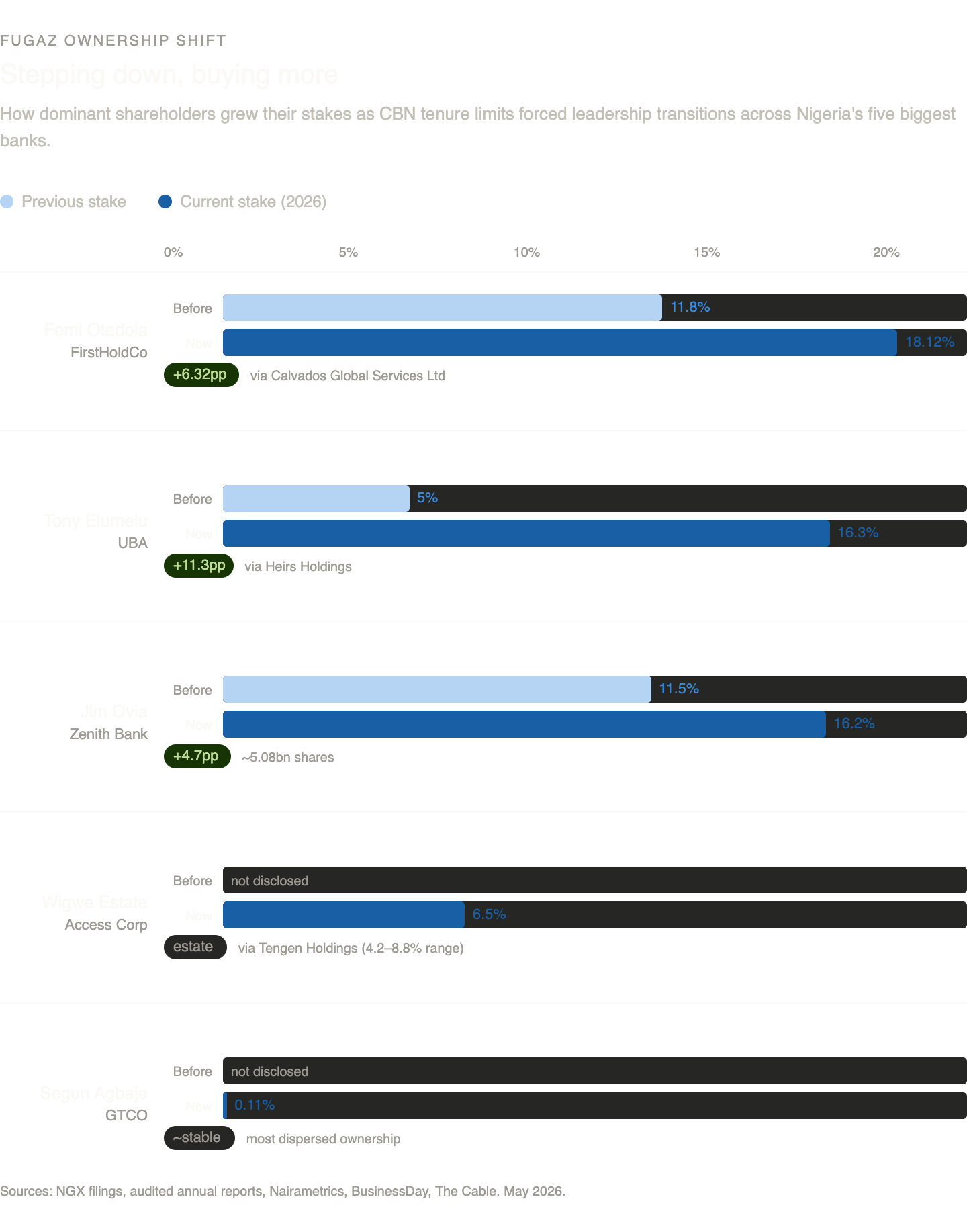

Ovia now holds approximately 16.2% of Zenith Bank, equivalent to around 5.08 billion shares, up from the 11 to 12% range disclosed in 2024 filings. He is the single most consequential shareholder in the institution he founded, and he holds that position more firmly today than at any point before he stepped down as chairman.

The CBN’s tenure rule changed his title. It did not change his exposure to Zenith’s future, and in the period surrounding his formal exit, he made certain of that.

The rule that set everything in motion

The CBN’s governance framework did not arrive quietly. When regulators embedded tenure limits into the supervisory architecture of Nigerian banks, the intention was clear: prevent long-term entrenchment from concentrating too much institutional power in too few hands for too long.

Twelve years for chairmen and key executives. No ambiguity, no extensions.

For a long stretch, this rule sat in the background while Nigeria’s Tier-1 banks expanded across the continent, grew their balance sheets, and cemented their dominance as the most systemically important financial institutions in sub-Saharan Africa.

The FUGAZ banks, representing First Bank under FirstHoldCo, United Bank for Africa, Guaranty Trust, Access, and Zenith, scaled fast enough that regulatory succession timelines felt distant.

They are no longer distant. Across all five institutions, founder-era and long-tenure leadership is cycling out of formal roles or approaching the point where it must. And the ownership data from the most recent filings reveals a pattern that the tenure framework was not designed to address: the men leaving the chairs are deepening their financial grip on the banks at the same time.

Zenith and UBA: 16% tells the real story

Ovia’s position at Zenith and Tony Elumelu’s position at UBA are now structurally similar in scale, even though they arrived there through different routes.

At Zenith, Ovia holds 16.2%, around 5.08 billion shares, a stake that grew from the 11 to 12% range recorded in 2024. The increase was not passive. It reflects deliberate accumulation in the period surrounding a formal governance transition, which raises a straightforward question about what the tenure framework is actually designed to prevent.

Zenith is among the most profitable banks in Nigeria, with total assets in the upper range of the Tier-1 group and dividend yields that have consistently ranked among the sector’s highest. A 16.2% position in that institution is an active economic interest in one of the most valuable financial franchises on the continent.

At UBA, the story is as interesting.

Tony Elumelu’s consolidated stake now stands at 16.3%, approximately 5.6 billion shares, accumulated largely through Heirs Holdings. The starting point for that position, as recently as a few years ago, was around 5%.

That is a tripling of economic exposure to an institution in which Elumelu has long held informal influence, now backed by a shareholder position that rivals or exceeds those held by major institutional investors.

In both cases, the CBN’s tenure rule applies to formal leadership positions. It does not apply to share registers.

FirstHoldCo: 18.12% and a Chairman still buying

FirstHoldCo presents a different governance dynamic from the rest of the FUGAZ group, and the ownership data here is the most aggressive of the five.

Femi Otedola’s consolidated stake in FirstHoldCo now stands at 18.12%, representing approximately 8.02 billion to 8.05 billion shares accumulated through a combination of direct holdings of 3.25 billion shares, or roughly 7.31%, and indirect holdings of 4.8 billion shares, or roughly 10.81%, held through his investment vehicle Calvados Global Services Limited.

That position has grown from 11.8% in 2024, and the pace of accumulation has been deliberate, including a NGN14.8 billion share purchase in December 2025 alone. He is now Group Chairman and the largest individual shareholder in Nigeria’s oldest commercial bank.

Otedola has publicly stated his intention to push total investment in FirstHoldCo beyond NGN320 billion by the end of 2026, which would further widen the gap between his position and every other individual shareholder in the institution.

One qualification matters here. RC Investment Management Limited holds an institutional stake of approximately 23.47% in FirstHoldCo, which is larger than Otedola’s individual position. The distinction is between institutional and individual shareholding.

Otedola is the largest individual shareholder, with a position that is still growing. The overall shareholder structure remains contested in the sense that no single individual commands a majority, but the direction of Otedola’s accumulation is unambiguous.

What FirstHoldCo illustrates, more explicitly than any other bank in the FUGAZ group, is that the tenure framework and ownership accumulation are operating in parallel and on separate tracks. The CBN can define who chairs the institution. It cannot define how many shares that person buys while doing so, or after.

Access Corp and GTCO: The two banks without a dominant shareholder

The contrast between Access Corp and GTCO on one side and Zenith, UBA, and FirstHoldCo on the other is significant, and the ownership data makes it concrete.

At Access Corp, the most consequential shareholder block is the Wigwe family estate, holding between 4.2 and 8.8% through Tengen Holdings following the death of Herbert Wigwe.

That range reflects the ongoing complexity of estate management rather than a clean ownership position, and the fragmented nature of the remaining shareholder base means Access is genuinely operating without a dominant anchor shareholder in the way its peers have one. Succession here is being managed through institutional structure rather than personal continuity.

GTCO is the most dispersed of the five. Segun Agbaje, the chief executive, holds approximately 0.11% of the institution he leads. No insider holds a meaningful equity position. Ownership sits with institutional investors, pension funds, and foreign portfolio holders, with no individual capable of exerting the kind of shareholder pressure that Ovia, Elumelu, or Otedola can apply at their respective banks.

Control at GTCO is structural, maintained through holding company architecture and governance design rather than concentrated personal equity.

These two banks show what the CBN’s governance model looks like when ownership is genuinely dispersed.

The tenure rule and the ownership structure work in the same direction. At Zenith, UBA, and FirstHoldCo, they are pulling in different directions.

What the CBN’s tenure rule changes and what the share register reveals

The CBN’s tenure framework succeeded at the objective it was designed to achieve. The same individuals cannot occupy formal leadership positions at Nigerian banks indefinitely. That constraint is real, it is being enforced, and it has produced visible transitions across all five FUGAZ institutions.

What the share registers of those same institutions reveal is that the individuals most affected by the tenure rule have, in several cases, responded by strengthening their economic position in the banks they can no longer chair.

Ovia at 16.2%, Elumelu at 16.3%, Otedola at 18.12% and still buying: these are not the ownership profiles of men withdrawing from institutional influence. They are the profiles of men converting formal authority into financial authority.

The holding company structures that several FUGAZ banks adopted in recent years add another layer to this picture. Strategic decisions that fall outside the regulatory perimetre of the operating bank sit at group level, which the tenure framework does not reach in the same way. Compliance happens at the operating level. Influence persists at the group level and through the share register.

Across the FUGAZ group, the same institutions still dominate deposits and credit allocation in Nigeria. The same investor networks still shape long-term direction. What is changing is the mechanism through which the most consequential individuals maintain their connection to those institutions.

Formal titles are giving way to equity positions, and in at least three of the five banks, those equity positions have grown larger, not smaller, as the governance transitions have unfolded.

The CBN’s tenure rule moved Jim Ovia out of the chairman’s seat. The Zenith Bank share register shows exactly where he went.