The first quarter (Q1) of 2026 has been particularly challenging for the crypto sector. As the dust finally settles on the latest round of corporate earnings, a rather unsettling narrative is taking shape across major publicly traded Bitcoin companies. Beneath the glossy veneer of surging adoption metrics and soaring top-line revenues lies a brutal, unavoidable truth that scaling a digital asset firm in 2026 is an exceptionally expensive endeavour.

This reality was laid bare this week by two of the market’s highest-profile companies, painting a grim picture of an industry struggling to normalise its balance sheets against a backdrop of aggressive market volatility.

Look at American Bitcoin, the BTC mining company backed by the Trump family. The Nasdaq-listed firm’s SEC filing for Q1 on Wednesday presents a classic modern tech paradox. On the one hand, the company is expanding at a breakneck pace; first-quarter revenue climbed to $61.5 million, an impressive 400% increase from $12.3 million in the same period last year. Yet, this growth failed to translate into actual profitability. Instead, it missed analyst projections by a mile and resulted in an $82.1 million net loss.

This deficit cannot be attributed to a routine accounting anomaly. It is a glaring indicator of the intense operational friction baked into the current ecosystem. To capture market share and sustain such rapid scaling, firms are bleeding cash. The sheer cost of maintaining state-of-the-art mining infrastructure, retaining top-tier cryptographic talent, and navigating a tangled web of global regulatory compliance has completely eclipsed American Bitcoin’s revenue generation.

It points to a structural vulnerability within the space; the unit economics of aggressive expansion are deeply flawed right now. Growth is being subsidised by punishing losses, and the public markets are growing increasingly impatient with the setup.

However, American Bitcoin’s losses look entirely manageable when compared to MicroStrategy’s. In what feels like a watershed moment for institutional crypto strategy, the firm posted an eye-watering $12.5 billion loss for Q1. For a company that has long served as the gold standard for corporate Bitcoin conviction, a deficit of this magnitude has rattled even the most steadfast investors.

Also read: Bitcoin fell 23% in Q1 2026, but these ‘unknown’ crypto tokens made gains

Michael Saylor is considering selling Bitcoin reserves to cover dividends

Perhaps more alarming than the loss itself is the strategic pivot it seems to have triggered. The revelation that Michael Saylor is considering selling Bitcoin reserves to cover dividend payouts represents a fundamental fracture in the prevailing ‘never sell’ orthodoxy.

For years, relentless accumulation was the bedrock of the firm’s market valuation. Being forced to liquidate core holdings to service shareholder obligations suggests that liquidity pressures are finally cracking even the most resolute balance sheets. When the market’s primary accumulator signals a willingness to distribute from its treasury, it sends a chilling ripple through broader liquidity pools.

The culprit: Bitcoin’s underwhelming performance in Q1

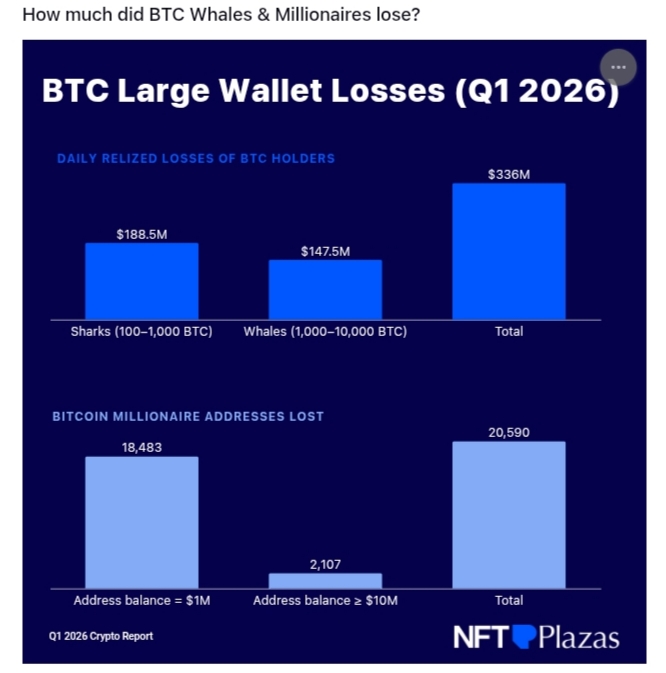

Crucially, these corporate balance sheets were not affected in isolation; they were battered by the underlying assets’ dismal performance. Bitcoin itself shed over 20% of its value during the period under review, creating a highly toxic environment for entities holding massive reserves. According to a recent Q1 2026 market report by NFT Plazas, large wallet holders, those commanding between 100 and 10,000 BTC, endured their worst quarter since the crypto winter of 2022, bleeding an average of $336 million daily.

Breaking those numbers down reveals a savage market contraction. ‘Sharks’ holding 100 to 1,000 BTC realised daily losses of roughly $188.5 million, whilst ‘Whales’ holding 1,000 to 10,000 BTC lost around $147.5 million a day.

Put together, the quarter saw a staggering $30.91 billion in total realised losses. These losses contributed to a severe drain in high-net-worth network participation. The number of Bitcoin millionaire addresses plummeted by 18,483, dropping to 113,233. Meanwhile, wallets holding $10 million or more shrank by 2,107.

To put that in perspective, Q1 2026 saw a 47.7% deeper year-on-year drop in millionaire addresses compared to the same period in 2025. This massive wealth destruction fundamentally eroded the capital base that traditionally props up corporate crypto valuations.

Overall, these metrics underscore a profoundly poor outing for the entire crypto sector in the first quarter. 2026 was supposed to usher in mature institutional integration and stabilised yields. Instead, it has been defined by defensive manoeuvring and historic cash burns. The industry is currently trapped in a transitional purgatory, too mature to be valued purely on speculative hype, yet far too volatile to generate the predictable cash flows demanded by traditional equity investors.

The grace period for loss-making crypto ventures is rapidly ticking, and the mandate for the rest of the year is clearly to find a path to operational efficiency or face an unforgiving market correction.