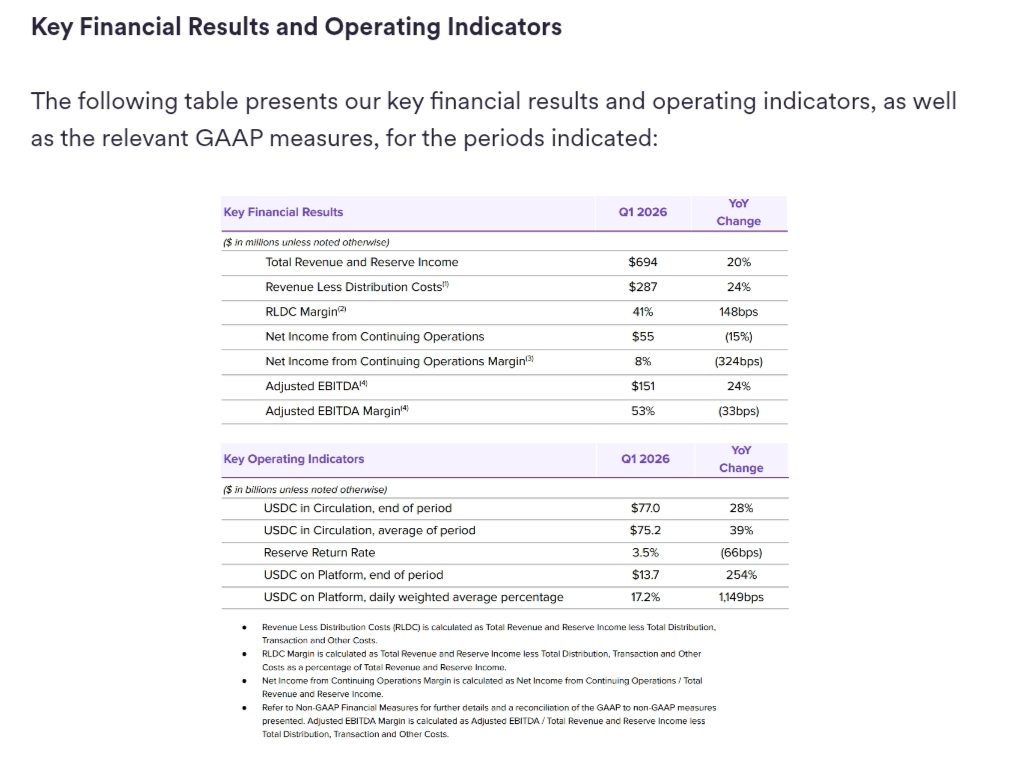

Circle Internet Financial, the firm behind the USDC stablecoin, announced on Monday that its first-quarter revenue for 2026 jumped 20% to $694 million, underpinned by a high-profile $222 million token sale linked to its forthcoming Arc network ecosystem. The company outperformed analyst projections across several key metrics, posting earnings per share (EPS) of 21 cents, comfortably ahead of the 17 cents expected by Wall Street, as it transitions from being a mere currency issuer into a primary builder of web3 infrastructure.

The quarterly results, published today, paint a picture of a company capitalising on its massive reserves to fund a pivot towards vertical integration. Alongside the revenue growth, Circle reported that its adjusted earnings before interest, taxes, depreciation and amortisation (EBITDA) rose 24% year-on-year to $151 million. While the company’s core business remains anchored in the digital dollar, these figures suggest a deliberate move to reinvest profits into proprietary technology rather than simply sitting on interest-bearing assets.

Market observers have long viewed stablecoin issuers as the plumbing of the digital asset world, necessary but largely invisible. However, the $222 million raised during the Arc network’s token presale indicates a change in status. The sale reportedly values the new blockchain ecosystem at $3 billion, providing Circle with a significant war chest to challenge established networks like Ethereum and Solana. By building its own rails, Circle is attempting to solve a long-standing dependency on third-party protocols that often suffer from congestion or fluctuating fees.

Also read: Coinbase posts second consecutive quarterly loss as stock falls 15%

Circle: From digital dollar issuer to network architect

This shift represents a fundamental change in Circle’s corporate strategy. For years, the company has operated as a tenant on other blockchains, minting USDC on various layers while remaining subject to the technical rules set by outside developers. The launch of the Arc network suggests that Circle is now ready to become a landlord. By controlling the underlying blockchain, the firm can offer a more seamless, compliant, and cost-effective environment for the institutional investors who already rely on its stablecoin for settlement.

The $3 billion valuation of the Arc project is particularly noteworthy given the current competitive landscape. It signals that private investors are betting on Circle’s brand of regulated innovation to win over traditional financial institutions. Unlike more decentralised but often opaque competitors, Circle has spent years cultivating a reputation for transparency and compliance in New York and Washington. The Arc network is expected to mirror this philosophy, providing a clean environment for the tokenisation of real-world assets, a market that many believe will be worth trillions by the end of the decade.

The $222 million injection will likely be channelled into aggressive developer grants and the construction of security protocols designed to prevent the exploits that have dogged other decentralised finance (DeFi) platforms. For Circle, the goal is not just to provide the money but to provide the entire vault. If it can successfully migrate a fraction of the existing USDC transaction volume to its own network, the revenue potential from transaction fees alone could dwarf its current earnings from interest income.

Also read: What Drift, Kelp DAO and Hyperbridge $600 million crypto hacks reveal about Web3 security

However, the move is not without challenges. Some industry purists argue that a blockchain controlled by a single corporate entity runs contrary to the decentralised ethos of the crypto market. There is also the significant technical hurdle of bootstrapping a new ecosystem from scratch. History is littered with Ethereum killers that failed to gain traction despite having hundreds of millions in funding. Circle will need to convince its existing partners that moving to the Arc network offers more than just a lower price point; it must offer a superior level of reliability.

The 20% revenue surge also reflects the broader recovery of the digital asset market in early 2026. As USDC adoption grows in cross-border trade and remittances, Circle is finding that its product-market fit is expanding beyond speculative trading. The company’s ability to beat EPS estimates by such a wide margin highlights efficient management of overheads even as it ramps up research and development spending.

As the year progresses, the focus will shift from these financial milestones to the technical delivery of the Arc network. If Circle can stick to its roadmap, the ARC token could become a central pillar of its business model, moving the company away from the volatility of interest rate cycles and toward a more predictable, software-as-a-service (SaaS) style of revenue. For now, the Q1 numbers indicate that Circle has the financial health and the market confidence to pursue this high-stakes evolution.