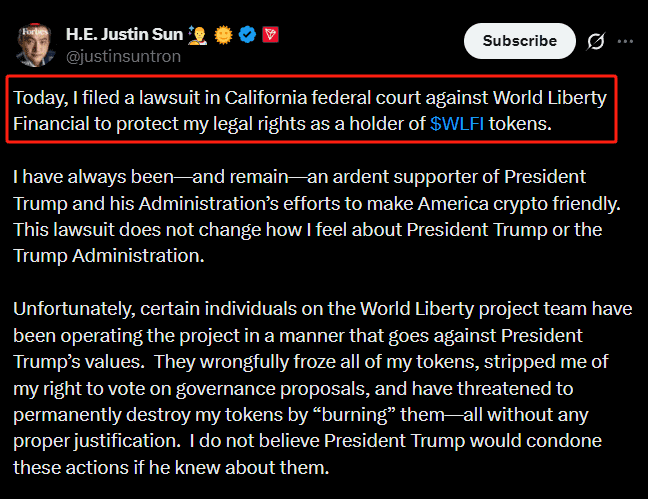

Tron founder and billionaire entrepreneur Justin Sun has formally filed a lawsuit against World Liberty Financial (WLF), a decentralised finance project closely linked to United States President Donald Trump. Filed in a California federal court on Tuesday, the lawsuit includes serious claims against the Trump-backed company, including extortion, fraud, defamation, and creating an “illegal scheme” to take Sun’s large digital asset holdings without his consent.

The legal action represents the boiling point of a months-long public feud over the governance and transparency of World Liberty Financial. Central to Sun’s grievance is the allegation that the DeFi protocol’s leadership fraudulently induced his initial investment in 2024 by actively soliciting his financial backing, only to later embed a covert “backdoor blacklisting function” within the platform’s smart contracts.

According to the court filings, this mechanism was subsequently weaponised to freeze his $WLFI tokens, stripping him of his governance voting rights and effectively rendering his multi-million-dollar investment hostage.

Justin Sun and the Trumps: A relationship turned sour

To understand the gravity of the lawsuit, one must look back to late 2024. At the time, Sun emerged as the largest publicly known investor in the then-fledgling World Liberty Financial, injecting tens of millions of dollars into the project and taking on an advisory role. Sun stated that his investment was a robust vote of confidence in the Trump family’s venture, viewing it as a cornerstone for making the United States a global, crypto-friendly hub.

However, the relationship was short-lived. Relations began to fray when Sun’s digital wallet, which reportedly held 540 million unlocked $WLFI tokens alongside a staggering 2.4 billion locked tokens, was frozen in September.

The platform’s developers allegedly activated the unpublicised administrative powers after Sun transferred a portion of his holdings to HTX, the crypto exchange he owns, and purchased a significant $100 million stake in a separate Trump-themed memecoin.

The complaint alleges that the WLF team not only restricted his assets but also resorted to coercive tactics. Sun claims the venture attempted to pressure him into further investments and demanded he promote their stablecoin across his Tron blockchain network, effectively using his frozen capital as leverage.

WLF: Earlier threats and public defamation

The lawsuit is not entirely unexpected, considering the bitter war of words that preceded it. The conflict spilled into the public domain earlier this month on the social media platform X. In a highly publicised spat, Sun accused the project of treating its investor community like a “personal ATM” and demanded transparency regarding who possessed the master keys to the restrictive smart contract.

In a swift and aggressive riposte, World Liberty Financial’s official account launched a blistering attack on Sun, accusing the billionaire of “playing the victim” to mask his own supposed misconduct. The project’s leadership publicly threatened Sun with legal action first, boldly declaring, “See you in court, pal. We have the evidence. We have the truth.”

Sun’s lawsuit now categorises these public outbursts, alongside the WLF team’s aggressive characterisations, as outright defamation designed to damage his professional reputation while obscuring the project’s own vulnerabilities. In his filing, Sun points to recent manoeuvres by WLF, such as taking out loans using $WLFI tokens as collateral, as evidence that the project is teetering on the verge of financial collapse and struggling to maintain liquidity. This comes as early retail investors in the project reportedly remain unable to trade 80 per cent of their tokens.

Still, Sun is careful not to offend Trump

Despite the severe allegations directed at the Trump-backed enterprise, Sun has been exceptionally careful to separate the project’s operational team from the US president himself. In a statement accompanying the lawsuit, Sun reaffirmed his unwavering support for Donald Trump’s broader crypto policy agenda. He expressed profound disappointment that certain individuals within the World Liberty team had engaged in behaviour fundamentally contrary to the president’s pro-business values, arguing that Trump would not tolerate such overreach if fully apprised of the situation.

Beyond the immediate financial damages, which Sun claims amount to hundreds of millions of dollars, the case is poised to serve as a landmark test for the broader decentralised finance sector. At its core, DeFi is built upon the promise of trustless, immutable infrastructure. The revelation that a major protocol could unilaterally deploy “freeze controls” challenges the very ethos of decentralisation. US federal courts will now have to determine the legality of such hidden administrative powers and whether they constitute a breach of contract or outright fraud.

Sun is asking the court to immediately unfreeze his tokens, award unspecified monetary damages, and permanently enjoin World Liberty Financial from acting on its threats to “burn” or destroy his trapped assets. For now, the global crypto industry watches closely as one of its most prominent figures takes a stand against a venture boasting the highest political connections in the land.