Transportation is a major player in the financial lives of young professionals in Nigeria’s big cities. It’s not just about getting from point A to point B, it’s about lifestyle, productivity, and opportunities.

Many see owning a car as a status symbol and a convenient option, but is it really worth it? With rising fuel costs, maintenance fees, and heavy traffic, it’s time to weigh the pros and cons.

Is owning a car an asset or a burden?

To this, a June 2025 report by Nigeria-based fintech Cowrywise titled “The Economics of Car Ownership in Nigeria” examines the financial and lifestyle trade-offs among three key transport options for young professions in Lagos, such as: “Owing a Car,” “Using ride hailing services” and, “Relying on public transportation.”

The study, through the lens of a hypothetical young professional, Sola, made an empirical analysis and case studies to determine which of the options best fit an average Nigerian income, lifestyle, and goals in the long run.

As each of the three options are alternative transportation channels, they come with associated real costs and benefits. This makes each a separate working formula to fit each individual’s tastes based on their financial capacity and smarter mobility decisions.

Also Read: Lagos ranked world’s fastest-growing tech city in 2025.

Associated costs of car ownership

From the Nigerian lens, the price of four Nigerian-used cars was deployed as a case study.

- Toyota Corolla 2005 – ₦4.0 million

- Kia Rio 2007 – ₦4.5 million

- Toyota Camry 2005 – ₦6.5 million

- Toyota Camry 2007 – ₦4.5 million

In the race for car ownership, Sola can either decide to own a car through saving to buy or borrowing to buy. Whereas both come with financial implications and lifestyle trade-offs.

Firstly, Sola could save ₦415,000 per month for one year (with an estimated 20% return), or ₦217,000 per month over two years (yielding approximately 16.5%).

Alternatively, Sola could fund the purchase through a combination of a staff loan (₦3 million at 15% per annum) and a digital loan (₦1.9 million at 84% per annum), resulting in monthly repayments of ₦575,000.

If Sola eventually purchases a clean Nigerian-used Toyota Corolla for ₦4.9 million (the estimated avg. cost of a Nigerian used car), other hidden costs are adding to the real cost of car ownership.

A maintenance cost of about ₦234,000 monthly or ₦2.8 million annually over five years sums her real cost to ₦22.7 million. Meanwhile, a resale value of ₦3.8 million can reduce the real cost to ₦18.9 million over the same period.

While car ownership comes with visible and hidden costs, it’s not entirely a losing game. Understanding replacement value can help individuals make more informed, long-term transportation decisions. As a car loses real value through depreciation, inflation, and exchange rate volatility, it may command a higher replacement cost over time.

However, the report concludes that owning a car is a great financial commitment.

For instance, to afford a used car of ₦4.9 million, Sola’s monthly budget for transport should fall within 10% to 15% of her income, based on the 50/30/20 budgeting rule, where 20% is for savings.

That means she will need to earn between ₦1.2 million to ₦1.5 million net per month. Notably, this kind of salary is earned by an Assistant Manager at a commercial bank. But Junior employees at oil companies earn that.

Associated cost for ride-hailing services

In another section, a typical Nigerian can choose to indulge in ride-hailing services for daily commutes to balance convenience, control, and cost. For this report, Bolt platform in Lagos was employed as a case study.

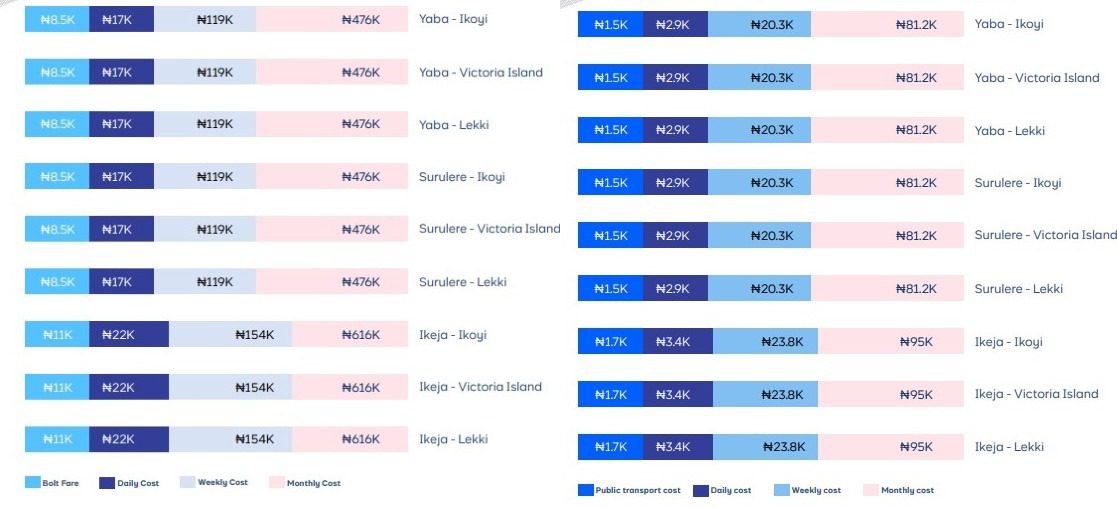

In major daily routes such as Yaba/Surulere to Ikoyi, Victoria Island, or Lekki, a bolt fare of two trips per day is estimated to cost ₦17,000 (₦8,500 per trip), ₦119,000 per week, and ₦479,000 per month.

For daily routes such as Ikeja to Ikoyi, Victoria Island or Lekki, a bolt fare of two trips per day is estimated to cost ₦22,000 (₦11,000 per trip), ₦154,000 per week, and ₦616,000 per month.

Ride-hailing apps like Bolt and Uber have transformed urban mobility in Lagos by offering a flexible alternative to car ownership. With 20 weekday and eight weekend trips each month, users like Sola, who want convenience, would incur a total transportation cost of about ₦461,176 monthly or ₦5.53 million annually.

When accounted for by increased pricing and fare variability, the long-term cost of ride-hailing in Lagos can potentially exceed the cost of owning a car.

Also, at ₦461,176 monthly or ₦5.53 million annually, Sola will need to earn ₦2.3–₦2.5 million net monthly to afford it sustainably.

The report explained that while ride-hailing requires no upfront investment (like that of car ownership) and eliminates maintenance worries, it comes with surge pricing, unreliable availability, and high long-term costs, often surpassing the price of owning a modest car.

Also Read: Beyond Uber and Bolt: Here are 5 lesser known e-hailing apps operating in Nigeria.

Associated costs with public transportation

In the last session, a typical young professional in Nigeria can choose to indulge in bus or danfo service for daily commute in the midst to balance affordability, accessibility, and consistent transportation means.

In major daily routes such as Yaba/Surulere to Ikoyi, Victoria Island, or Lekki, a bus fare of two trips per day is estimated to cost ₦2,900 (₦1,500 per trip), ₦20,300 per week, and ₦81,200 per month.

For daily routes such as Ikeja to Ikoyi, Victoria Island, or Lekki, a bus fare of two trips per day is estimated to cost ₦3,400 (₦1,700 per trip), ₦23,800 per week, and ₦95,000 per month.

Unarguably, public transportation remains the most cost-effective mobility option for Lagos residents. For commuters like Sola, relying on public buses or danfos for 20 weekday and 8 weekend trips each month would amount to just ₦115,000 monthly or ₦1.4 million annually (approximated for inflation).

The fee makes public transport significantly cheaper than ride-hailing or car ownership.

While public transport saves money, it demands a high trade-off in time, comfort, and security. Costs like frequent delays, overcrowding, and safety concerns often turn daily commutes into draining experiences. Despite its accessibility and low cost, public transportation may not meet the expectations of young professionals who value time, consistency, safety, and high control.

Again, for young professionals like Sola, the choice hinges on “to spend less and endure the stress”, or “to spend more for comfort and control.”

Transport trade-off: the real cost decision

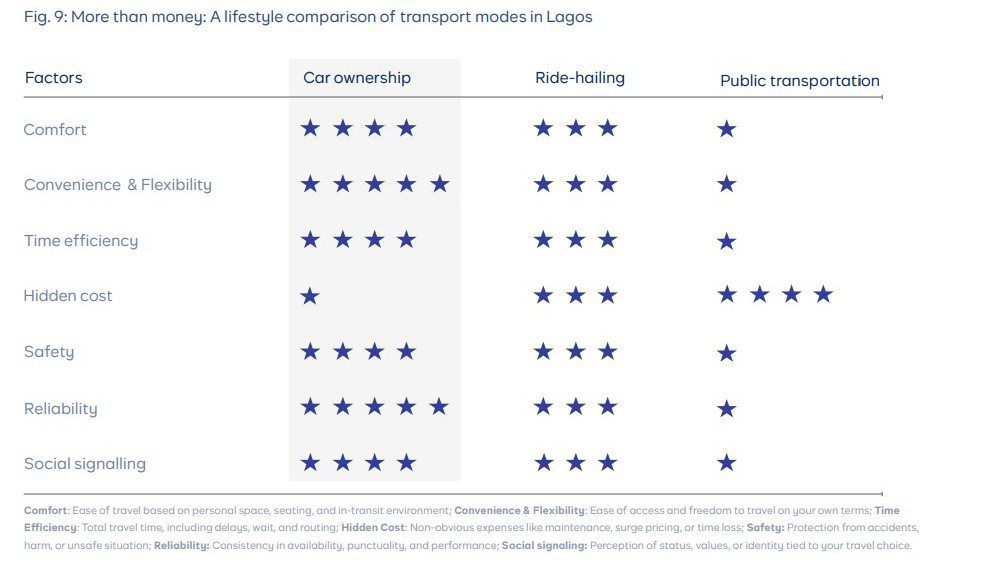

In comparison with cost metrics across the three options over the five years, deciding on public transport is the most affordable and cheapest (₦2.8 million). Though it comes with limited comfort, time inefficiencies, and safety risks.

For car ownership, it poses the highest upfront cost, financial commitment, and more stable long-term spend (₦5.5 million). However, it presents a significant level of comfort and control over lifestyle. Despite having no initial investment, ride-hailing holds the highest monthly and long-term cost (₦9.9 million). On the lighter end, the option offers a balance between convenience and flexibility.

The Cowrywise report explains that the best option still depends on individual priorities such as cost-efficiency, affordability, and level of convenience desired, or level of desire to control.

Getting a car: saving to buy or borrowing to buy?

Sola, newly promoted to Banking Officer, now earns ₦1,000,000 monthly (net) and wants to save for a car. Sola has two options.

- Save 42% (₦415,525) of her income per month and get a car of ₦5.5 million at the end of the year (which can be tough) or save 22% (₦217,573) of her income per month and get a car of ₦6.1 million (adjusted for inflation) at the end of the second year.

- Sola could buy the car now for ₦4.9 million by taking a staff loan of ₦3 million (3x her salary) at a 15% annual rate for one year. And borrow the remaining ₦1.9 million from family and friends or use digital lending apps at 4%–10% monthly, equivalent to about 84% annually.

However, the report explained that saving for over two years is the most financially responsible option, especially as it aligns with personal finance principles. Meanwhile, borrowing introduces repayment pressure, and combining staff loans with family support might not always be accessible.

For individuals deciding not to own a car, it affects their quality of life, productivity, health, and career growth.

Also Read: Opay, PalmPay, or Moniepoint? Here are the top POS operators in 5 major Lagos markets.

Experts’ opinion: the final trade-off decision

The decision to own a car, take a ride-hailing service, or use public transport can be a life-determining factor. Owing to this, the report, based on financial experts, made some measurable considerations for young professionals to weigh their transportation decisions.

- Transportation costs should be between 10% and 20% of your monthly income. Young professionals trying to stabilise their income should opt for either public transport or ride-hailing services.

- Perhaps your daily commute includes routes or neighbourhoods where safety is a concern; protecting your peace of mind should be the priority. In such cases, opting for ride-hailing apps or a personal vehicle may be worth the extra expense.

- If you’re planning to start a family soon, owning a car can make daily life far easier for school runs, errands, and weekend outings.

- If you desire utmost comfort and driving makes you happy, boosts your confidence, and fits your lifestyle, getting a personal car is welcomed in line with affordability.

- Young professionals’ transportation choice should reflect not just their current needs, but also their life plans.

In short, the trade-off decision cuts across affordability, convenience, and choice of lifestyle.