Nigeria’s rapid embrace of stablecoins has become one of the clearest examples of how digital finance is reshaping emerging markets. But the International Monetary Fund (IMF) has now flagged the trend as a serious macroeconomic risk. In its latest Article IV consultation, the IMF argues that the country’s heavy use of dollar-pegged tokens such as USDT and USDC may be driving a quiet form of digital dollarisation, one that could weaken the naira and reduce the effectiveness of domestic monetary policy.

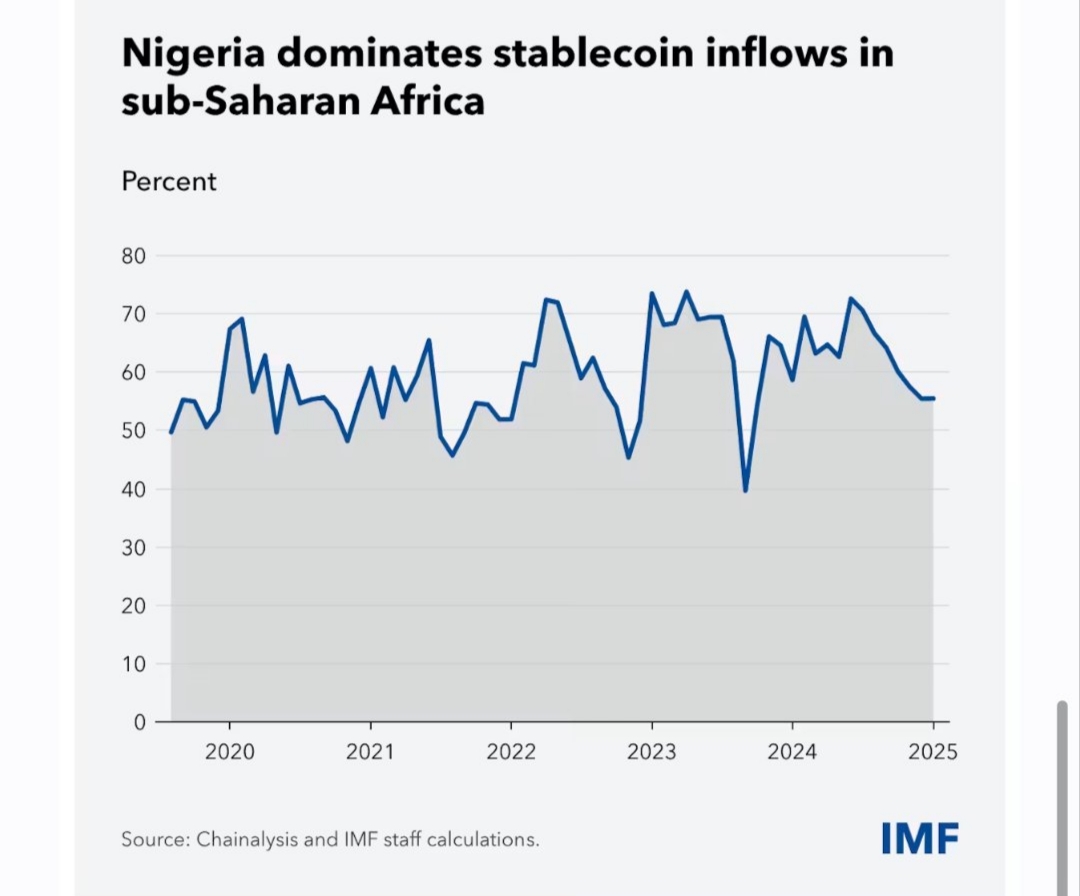

The scale of the shift is difficult to ignore. Quoting Coinanalysis data, the IMF pointed out that Nigeria accounted for around 60% of stablecoin inflows into sub-Saharan Africa between mid-2023 and mid-2024. The broader market linked to this activity is estimated at $59 billion, underscoring how quickly stablecoins have moved from a niche crypto product to a practical financial tool used by everyday individuals, traders and businesses alike.

For many Nigerians, the appeal is obvious. The naira has faced sharp depreciation, inflation has remained high, and access to foreign exchange has been constrained. This makes stablecoins overtly attractive, offering something the formal financial system has struggled to provide: speed, predictability and access to dollar liquidity. A smartphone and internet connection are often enough to send, receive or store value outside the local banking system. For small businesses that need to pay suppliers abroad, stablecoins can be a lifeline. For families receiving remittances, they can reduce delays and cut costs.

That practical utility is central to the boom. Traditional remittance routes into sub-Saharan Africa remain expensive, with fees that can average around 9% of the transaction value. Stablecoin transfers, by contrast, can be faster and cheaper. They help users bypass bank queues, foreign exchange bottlenecks and settlement delays. In many cases, they function as a parallel payments rail for people who have little faith in the pace or reliability of conventional channels.

The dangers of unchecked dollar-pegged stablecoins

Yet the same features that make stablecoins useful also make them troubling for regulators. The IMF’s concern is not simply that people are using crypto. It is that a large share of everyday commerce, savings and cross-border trade may be migrating into a dollar-denominated digital layer that sits outside the country’s monetary controls. When money increasingly moves through a system pegged to the US dollar rather than the naira, the nation’s legal tender, the central bank’s ability to steer the economy becomes weaker. Interest rates, liquidity measures and exchange-rate policy all lose some of their influence if businesses and households are already operating in a shadow dollar economy.

There is also the issue of financial transparency. As activity shifts away from commercial banks and into decentralised wallets, peer-to-peer platforms and offshore exchanges, authorities face a growing blind spot. Transactions may be harder to trace, especially when they move across informal channels. That raises the risk of illicit financial flows and complicates anti-money laundering enforcement. The very design that makes crypto flexible can also make oversight far more difficult.

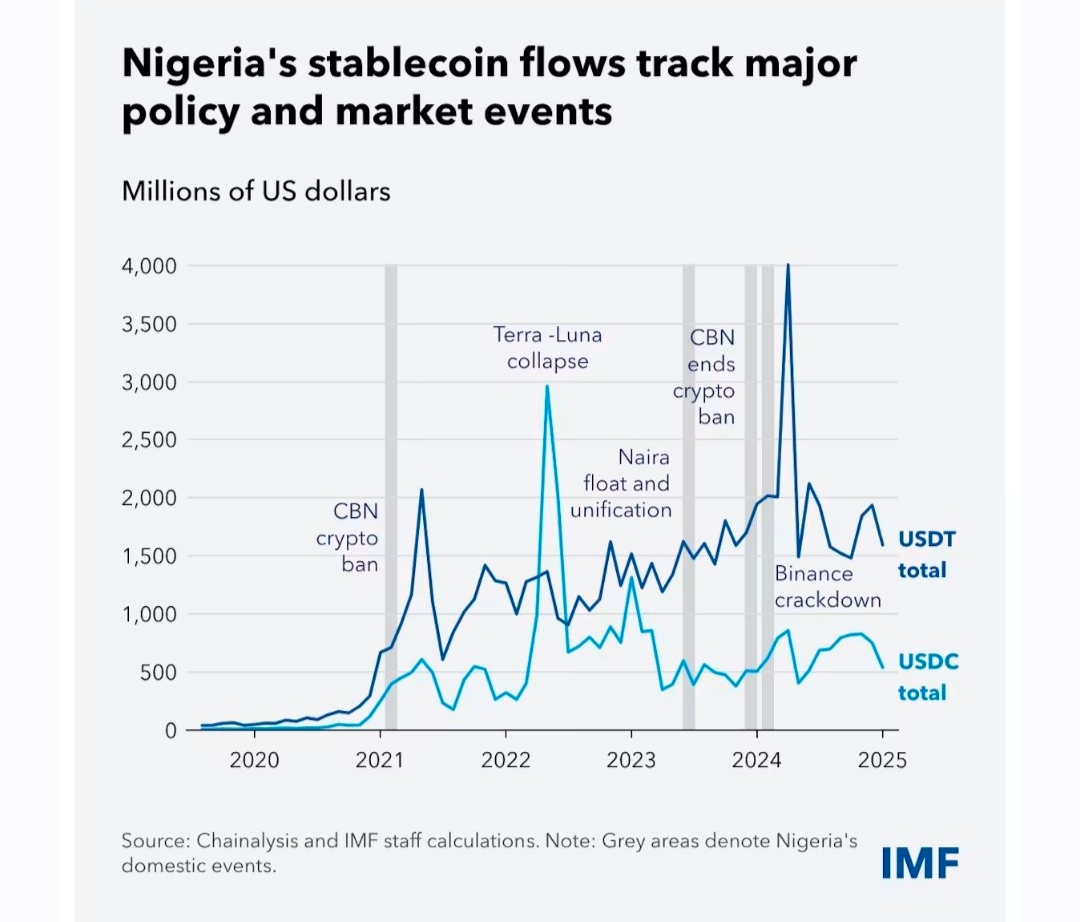

The IMF is not calling for a blanket ban. Nigeria has already seen how restrictive measures can simply push activity underground. After the Central Bank’s 2021 restrictions on banks serving crypto exchanges, much of the market shifted to more informal and less regulated peer-to-peer channels. The lesson, according to the IMF, is that prohibition alone does not solve the problem.

The IMF’s four-point policy blueprint

Instead, the Fund is urging a more measured policy response. First, it argues that Nigeria must rebuild confidence in the naira by tackling inflation, improving macroeconomic stability and making the foreign exchange market more transparent. A stronger domestic currency would naturally reduce the demand for digital dollars.

Second, regulators need a clearer framework for stablecoins, wallets and exchanges. Rather than forcing these actors outside the system, the goal should be to bring them within a proportionate regulatory perimeter, with strong consumer protection and strict compliance standards.

Third, the formal payment system must improve. If banks and payment providers can offer faster, cheaper and more reliable cross-border transfers, they will be better placed to compete with crypto networks. The IMF has also pointed to the eNaira as a potential state-backed digital alternative, though its success would depend on usability, trust and real-world relevance. A problem that the apex bank has since realised and is trying to fix with its recent Payments System Vision 2028 (PSV 2028).

Finally, the report calls for stronger surveillance. Authorities will need better blockchain analytics, closer coordination with global financial intelligence partners and more advanced tools to monitor on-chain flows. Without that visibility, regulating a fast-moving stablecoin market will remain extremely difficult.

Nigeria’s stablecoin surge is arguably the most significant shift in African fintech right now. However, turning this unprecedented capital inflow from a macroeconomic vulnerability into a sustainable economic driver requires a highly strategic regulatory pivot. The technology has already taken root; it is now up to the policymakers to build an infrastructure that can handle it safely.